.avif)

Investing in real estate is one of the most effective ways to grow wealth, and leveraging your existing home equity through a Home Equity Line of Credit (HELOC) can be a smart and flexible financing strategy.

A HELOC allows homeowners to tap into the equity they’ve built in their current property and use it to fund the purchase of another one - whether it's a second home, rental property, or vacation getaway.

.avif)

What is a Home Equity Line of Credit (HELOC)?

Think of it like a credit card, but it’s tied to your house. When you own a home, you build up something called “equity.” Equity is the difference between how much your home is worth and how much you still owe on your mortgage.

A HELOC allows you to borrow money against this equity. You don’t have to sell your house to get the cash. You can borrow a portion of your equity through a flexible line of credit. You can use this money however you like — including buying another property.

How Does a HELOC Work?

A HELOC allows you to borrow money using the equity in your home. To understand how it works, let’s go through a simple example.

Imagine your home is currently valued at $400,000. You still owe $200,000 on your mortgage. This means you have $200,000 in home equity (which is the difference between your home’s value and what you owe).

Most banks will let you borrow up to 80% of your home’s value. Here’s how the calculation looks:

- 80% of $400,000 = $320,000

- Subtract your current mortgage balance of $200,000

- That leaves you with access to up to $120,000 through a HELOC

This $120,000 becomes your flexible line of credit. You can borrow from it whenever you need, similar to using a credit card - but the big advantage is that HELOC interest rates are much lower than credit cards or personal loans. On the flip side, the debt is secured by an in interest in your home, which is why the rate is lower.

This way, you can tap into your home’s equity without selling your house and use it for your next property purchase!

What Can You Do With Your HELOC?

Your home equity is a hidden superpower and HELOC is the key to unlocking it. Here are three smart ways you can use a HELOC:

1. Consolidate Debt

If you’re carrying credit card balances, personal loans, or other high-interest debt, a HELOC can help you save money. Since HELOCs typically offer much lower interest rates compared to credit cards, you can use it to pay off your debts in one go and reduce your monthly payments. Imagine having just one easy payment with a lower interest rate - more money in your pocket each month!

2. Access Liquidity

Sometimes, life happens, and you need quick access to cash. Whether it’s for home renovations, medical expenses, or an emergency fund, a HELOC gives you flexibility. You don’t have to use it all at once; you borrow only what you need, when you need it. Think of it like a financial safety net you can tap into anytime.

3. Reinvest into Real Estate

This is where it gets exciting. You can use your HELOC as a down payment or even for the full purchase of your next property. Whether you’re buying a rental property, a vacation home, or flipping houses, using your home equity lets you build your real estate portfolio without touching your savings.

How to Use a HELOC to Buy Another Property?

Let’s break it down step by step so it’s super easy to follow. Here’s exactly how you can use a HELOC through Altgage to help you buy your next property:

Step 1: Track Your Home Equity

The first thing you need to do is find out how much equity you have built up in your current home. This is where Altgage makes things really easy. With our simple online tools, you can track your home equity in real-time without any hassle.

By knowing exactly how much your home is worth and how much you still owe on your mortgage, you’ll get a clear picture of the amount you can borrow.

Why this matters: By tracking your equity, you’ll have a clear idea of your borrowing power, helping you plan your next property purchase with confidence.

Step 2: Apply for a HELOC

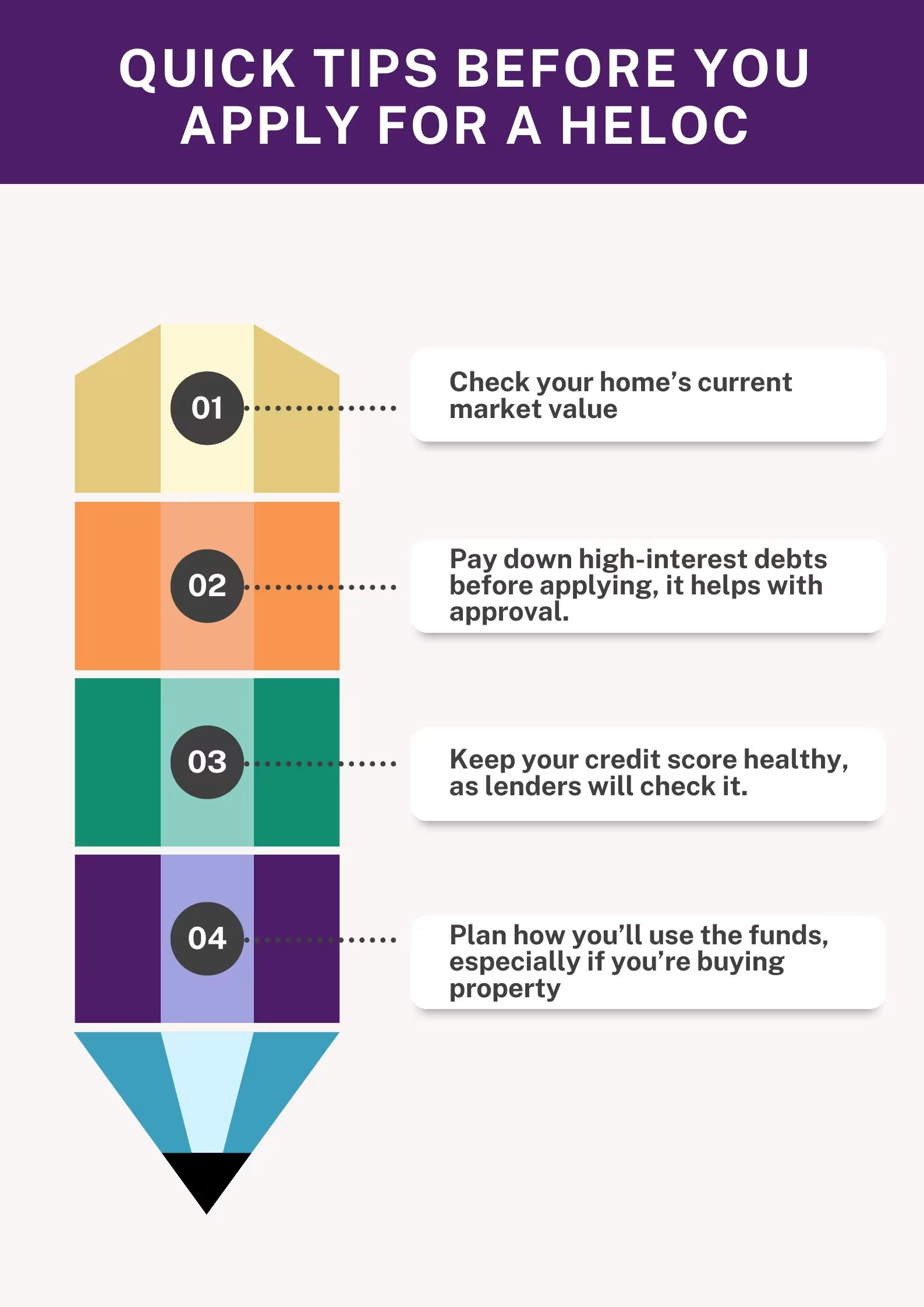

Once you know how much equity you have, it’s time to apply for a HELOC. At Altgage, we make the application process simple and straightforward, offering competitive rates and flexible terms. When you apply, we’ll review a few basic things like your home’s current value, your credit score, how much you still owe on your mortgage, and your overall financial picture.

The best part is - we guide you through every step, so you don’t have to stress about complicated paperwork. Getting pre-approved with Altgage gives you a clear understanding of how much you can borrow to fund your next property purchase.

Step 3: Get Access to Your Credit Line

After your HELOC is approved, you’ll receive access to a credit line based on your home equity. Think of it like a credit card, but with much lower interest rates and higher borrowing limits. You don’t have to take out all the money at once. Instead, you can borrow only what you need and use it when you’re ready.

As you pay off the amount you’ve borrowed, you can access that money again in the future. It’s a flexible, revolving credit line that can support your real estate goals both now and later.

Step 4: Use HELOC for Your Next Property

Now comes the exciting part - actually using the HELOC to buy your next property. You can use the funds from your HELOC to cover the down payment on your next home or even buy a smaller investment property outright, depending on the amount you qualify for.

Many people also use a HELOC to invest in rental properties, vacation homes, or flip houses. Another smart move is to use part of the HELOC for your down payment and keep some funds aside for repairs, renovations, or closing costs.

Step 5: Repay Smartly

Repaying your HELOC is more flexible than a traditional loan. You only have to pay interest on the money you actually use, not the total credit limit. Plus, most lenders offer an interest-only payment period during the first few years, which keeps your monthly payments low. This helps you stay comfortable while your investment property starts generating income or increases in value.

Later, you can start paying down the principal at your own pace, and many HELOCs don’t have penalties for early repayment. With smart planning, you can make your HELOC work for you without feeling financially stressed.

With a HELOC, you can turn your home equity into a tool for financial freedom—whether it’s paying off debt, handling emergencies, or buying your next property. Altgage is here to help you track, access, and invest your home equity with ease.

👉 Ready to see how much home equity you have?

Visit Altgage and track your home equity today. Your next property could be just a few clicks away!

Invest smart. Use equity wisely. Build wealth through strategic property acquisitions.