.avif)

If you've read our guide on what a rapid rescore is and how it works, you know the mechanics. Now the question that actually matters: how much will it improve your score?

The honest answer: 20 to 100 points for most borrowers, with some seeing more and some seeing less. The range is wide because the result depends entirely on what's dragging your score down and what you can fix.

Here's how to figure out where you'll land.

Why Your App Score and Mortgage Score Don't Match

Before we talk about improvement, you need to understand what's being improved. Your mortgage lender uses FICO models 2, 4, and 5 — older, industry-specific models pulled from all three bureaus. They take the middle score. The VantageScore or FICO 8 your banking app shows can be 20–80 points higher.

Here's how the two models weigh your credit differently:

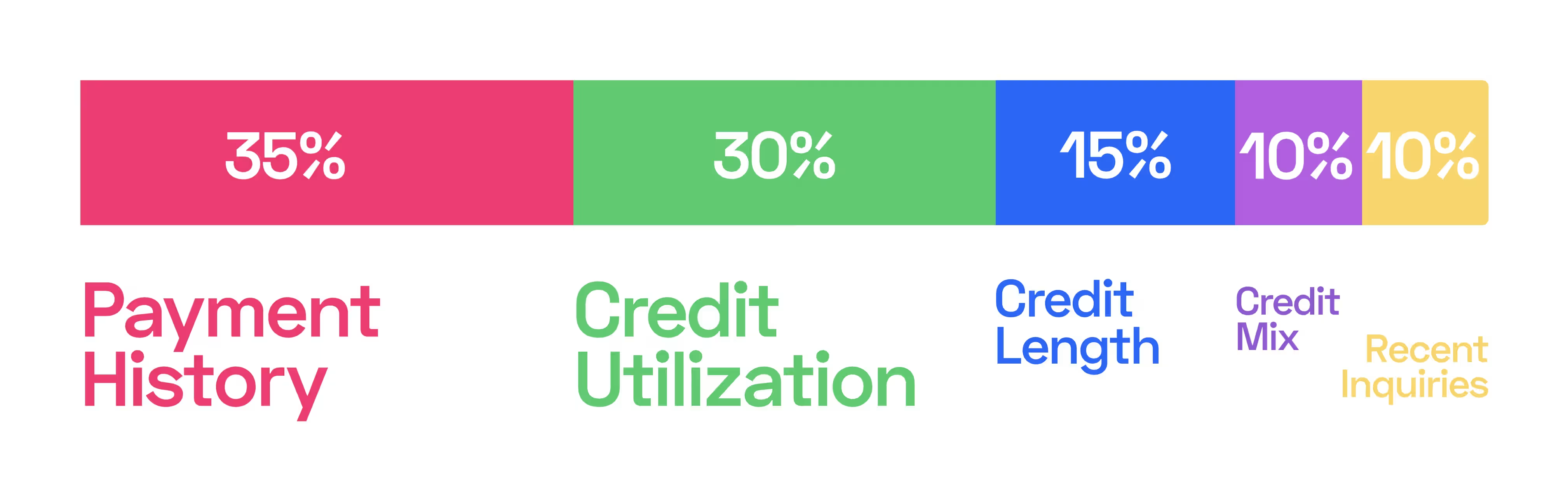

FICO (mortgage version): Payment history 35%, credit utilization 30%, credit length 15%, credit mix 10%, new inquiries 10%.

VantageScore 3.0 (your app): Payment history 40%, age and type of credit 21%, credit utilization 20%, balances 11%, recent credit 5%, available credit 3%.

The key difference: FICO weighs utilization at 30% vs VantageScore's 20%. That's why paying down credit cards moves your mortgage score more dramatically than what your app predicts. For a deeper explanation, read Mortgage Credit Score vs Consumer Credit Score.

The Factors That Respond to a Rapid Rescore

Not all score factors can be rescored. Credit Utilization is the biggest levers. Payment history only matters when correcting an error like a misclassfied late payment. Lenght of credit history is only affected when adding or removing authorized users. Credit Mix and New inquiries do not impact a rapid rescore.

Utilization is the engine of most rescore improvements. If your score is low because of high card balances, a rescore after paydown delivers the biggest gains. If your score is low because of late payments or short history, the improvement will be modest.

Improvement Ranges by Borrower Profile

These ranges are based on Altgage's Rapid Credit Boost program (80%+ success rate):

Profile 1: The High-Utilization Borrower

Starting score: 660–710. Problem: Credit card utilization above 50%, sometimes above 80%. Often self-employed borrowers running business expenses through personal cards. Action: Pay down all cards to below 10% utilization. Typical improvement: 40–80 points.

This is the most reliable and dramatic rescore outcome. A borrower at 78% utilization who drops to 8% will almost always see a significant jump.

Profile 2: The Thin-File Borrower

Starting score: 670–720. Problem: Fewer than 5 accounts, short average account age. Common with younger buyers and recent immigrants. Action: Add as authorized user on a well-managed account (high limit, low balance, 5+ year history). Typical improvement: 20–45 points.

Profile 3: The Error Correction

Starting score: Varies widely. Problem: Incorrect balance, duplicate account, wrong late payment record, account that doesn't belong to borrower. Action: Correct the error with documentation, rescore to update. Typical improvement: 20–50 points (sometimes more).

Profile 4: The Paid Collection

Starting score: 580–680. Problem: A collection account that's been paid off but still shows as outstanding. Action: Provide payoff letter, rescore to update status. Typical improvement: 15–40 points.

Profile 5: The Harmful Authorized User

Starting score: 680–720. Problem: Borrower is an authorized user on someone else's account with high utilization or late payments. Action: Remove self from the account, rescore. Typical improvement: 10–25 points.

Profile 6: The Already-Optimized Borrower

Starting score: 730+. Problem: Low utilization, long history, no errors. Action: Limited. Typical improvement: 0–15 points.

If your credit is already clean and well-managed, there may not be enough room for a meaningful improvement. We'll tell you this upfront.

What About the Other 20%?

Our 80%+ success rate means roughly 1 in 5 borrowers doesn't see a meaningful improvement. Here's why:

No fixable issues exist. The score is low due to legitimate, accurate negative marks — recent late payments, active collections, a bankruptcy still within the reporting window. A rescore can't change accurate negative information.

The improvement isn't enough to cross a threshold. A borrower at 695 might get a 15-point boost to 710, but if the meaningful threshold is 740, the improvement doesn't change their loan terms enough to matter.

Documentation issues. The creditor's balance letter has contingency language, isn't on proper letterhead, or the creditor won't provide documentation in the format the bureaus require.

Timing conflicts. A new negative item posts between the simulation and the rescore, offsetting the gains.

We're transparent about these limitations because false expectations help nobody. When we run the simulation, we'll tell you the honest projected outcome — including if it's not likely to move the needle.

How Long Until the Improvement Shows?

A Rapid rescore (through lender) takes 3–14 business days. Standard credit reporting cycle30–45 days. Credit bureau dispute resolution takes 30–45 days. Finally, credit repair (removing negative items) takes 3–12 months

The rescore updates your mortgage credit report specifically. The consumer scores you see on banking apps may take longer to reflect the same changes.

Translating Points Into Dollars

Score points matter because they translate directly into money. Here's what key threshold crossings mean on a $350,000 conventional loan with 5% down:

A jump from 700 → 740 saves $164/month or ~$9,840 over 5yrs. A jump from 680 → 720 saves $192/month and ~$11,520 over 5yrs. A jump from 660 → 700 saves ~$174/month or ~$10,440 over 5yrs

For the full breakdown of how credit score impacts rate and PMI pricing, read How Much Does a Credit Score Boost Save on a Mortgage?

Frequently Asked Questions

Is a 100-point improvement realistic?

It's possible but at the high end. We see it most often with borrowers who have very high utilization (70%+) across multiple cards AND a harmful authorized user or error. More typical is 30–60 points.

Can a rapid rescore get me from 580 to 620?

If the gap is driven by high utilization or an error, yes — that 40-point jump is well within the typical range. If the gap is driven by recent late payments, probably not.

How many times can I do a rapid rescore?

Typically one per file per mortgage application. This is why bundling all improvements into a single rescore is critical.

Does the improvement last?

Yes — as long as the underlying changes remain in place. If you paid your cards down for the rescore and then run them back up, your score will drop at the next reporting cycle. Maintain the changes through closing and beyond.

What if the rescore doesn't help enough?

If the simulation shows the improvement won't cross a meaningful threshold, we may recommend waiting and addressing credit repair issues first, adjusting the loan program (FHA vs conventional), or exploring other compensating factors.

The Bottom Line

A rapid rescore delivers 20–100 points for most borrowers, driven primarily by utilization paydown, authorized user optimization, and error correction. The biggest gains go to borrowers with fixable issues — high balances, outdated data, or toxic authorized user accounts.

If your score is within striking distance of a threshold that matters (620, 680, 700, 740, 760), a rescore can close the gap in under two weeks. If your score is held back by legitimate negative marks, a rescore alone won't be enough — but it can be the final step after credit repair has done the heavy lifting.

Altgage's Rapid Credit Boost is free, runs a simulation before committing, and has an 80%+ success rate. Check live rates at rates.altgage.com, or get pre-approved.

Related Reading on Altgage

- How to Boost Your Credit Score for a Mortgage (Fast)

- What Is a Rapid Rescore? Can I Do It Myself?

- How Much Does a Credit Score Boost Save on a Mortgage?

- 5 Fastest Ways to Boost Your Credit Score Before a Mortgage

- Credit Boosting vs. Credit Repair

- Why Is My Credit Score Different on Different Sites?

- Get Your Rate →

- Get Pre-Approved →