.avif)

Did you know that buying a home in Massachusetts could lower your tax bill? Many homeowners are unaware that mortgage interest, property taxes, and even certain home improvements may qualify for valuable tax deductions or credits. Understanding these benefits can help you save thousands of dollars each year.

In this article, we’ll explore the major tax benefits of homeownership in Massachusetts, how they work, and what homeowners should know when filing their taxes.

1. Mortgage Interest Deduction

One of the most significant tax benefits for homeowners is the mortgage interest deduction. When you purchase a home using a mortgage, a portion of your monthly payment goes toward interest, which may be deductible on your federal tax return.

Homeowners who itemize deductions can deduct mortgage interest paid on qualified loans used to buy, build, or improve their primary or secondary home. Interest paid on mortgages up to $750,000 of debt qualifies for this deduction.

For many homeowners, especially during the early years of a mortgage, interest payments can be substantial. Deducting this interest can reduce taxable income and result in significant tax savings.

Note: To claim the home mortgage interest deduction, the loan must be secured by a qualified home. This can include your primary residence or a second home. Eligible properties may include a house, condominium, cooperative, mobile home, house trailer, boat, or any similar property that has sleeping, cooking, and toilet facilities.

Source: https://www.irs.gov/publications/p936

2. State and Local Tax (SALT) Deduction

Another major tax advantage is the State and Local Tax (SALT) deduction, which allows homeowners to deduct certain taxes paid to state and local governments.

This includes:

- Local property taxes

- State income taxes or sales taxes

Under federal tax rules, these combined deductions were limited to $10,000 per year till 2024 for married couples filing jointly; however, under the “big beautiful bill” taxpayers can now claim up to $40,000 in State and Local Taxes, which are primarily real taxes.

Should Massachusetts homeowners itemize deductions?

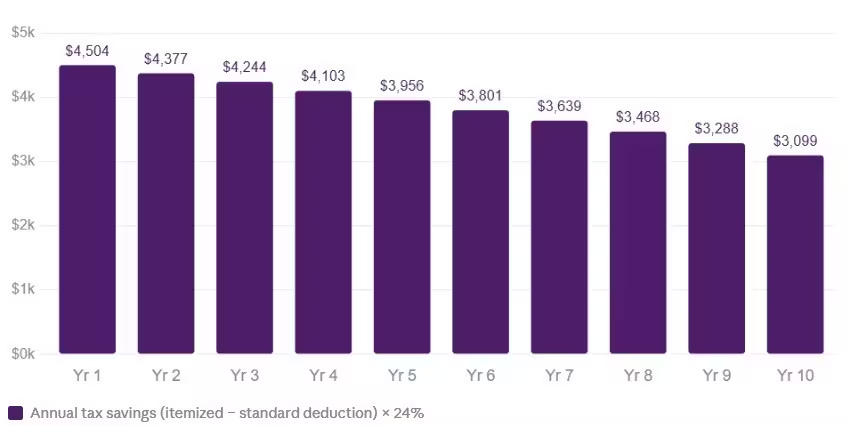

For many homeowners, the answer is yes but it depends on your mortgage size, property tax bill, and income. To understand how it works, here's a real-world example using a $250,000 household income and a $700,000 mortgage.

The 2025 standard deduction for married couples filing jointly is $31,500. But a Massachusetts homeowner with this mortgage can claim:

Mortgage interest (year 1): $35,000

Property tax (1.5% of $700,000): $10,500

Other deductions (charity, childcare): $5,000

Total itemized: $50,500

That's $19,000 more than the standard deduction. At a 24% federal marginal tax rate, that gap translates to roughly $4,560 in annual tax savings.

One important recent change: the SALT deduction cap was raised to $40,000 in 2025, up from $10,000, meaning Massachusetts homeowners can now deduct their full property tax bill alongside state income taxes.

As the chart shows, this advantage narrows over time as mortgage interest decreases. But over 10 years, a homeowner in this scenario could save approximately $36,000 compared to taking the standard deduction every year.

3. Mortgage Interest Credit (For Qualified Homeowners)

Some homeowners may qualify for the Mortgage Interest Credit, which is designed to help low and moderate-income families afford homeownership. This credit is available to homeowners who receive a Mortgage Credit Certificate (MCC) issued by a state or local government agency.

Generally, an MCC is issued in connection with a new mortgage used to purchase a primary residence. The certificate specifies the credit rate and the certified indebtedness amount, and only the interest paid on that certified amount qualifies for the credit.

Eligible homeowners can claim a portion of the mortgage interest they pay each year as a tax credit rather than a deduction, which can directly reduce the amount of tax owed.

Note: Homebuyers must contact their state or local housing finance agency before obtaining a mortgage to determine whether MCCs are available and to apply for the certificate. Because credits directly reduce tax liability, this benefit can be particularly valuable for qualifying homeowners.

Source: https://www.irs.gov/publications/p530

4. Energy-Efficient Home Improvement Tax Credits

Massachusetts homeowners who invest in energy-efficient upgrades may also qualify for federal energy tax credits.

Eligible improvements may include:

- Solar panel installations

- Energy-efficient windows or insulation

- High-efficiency HVAC systems

Homeowners may be able to claim up to 30% of the cost of certain qualified energy upgrades, helping offset the expense of improving their home’s energy efficiency.

These incentives not only lower taxes but also reduce long-term energy costs.

5. Senior Circuit Breaker Tax Credit in Massachusetts

Massachusetts offers a unique tax benefit known as the Senior Circuit Breaker Tax Credit.

This program is designed to help seniors who face high property tax burdens. Eligible residents who are 65 or older may claim a refundable tax credit based on the real estate taxes they pay on their primary residence.

For the 2025 tax year, the maximum credit is $2,820, and if the credit exceeds the taxpayer’s tax liability, the remaining amount may be refunded.

To qualify, applicants must meet certain income limits and property value thresholds established by the state.

6. Capital Gains Tax Exclusion When Selling a Home

Homeowners may also benefit from tax advantages when selling their property.

If the home is your primary residence and you meet certain ownership and residency requirements, you may exclude a portion of the profit from federal capital gains tax.

Current rules allow homeowners to exclude:

- Up to $250,000 of profit for single filers

- Up to $500,000 for married couples filing jointly

This exclusion can significantly reduce the tax impact when selling a home after it has appreciated.

7. Long-Term Financial and Wealth-Building Benefits

Beyond direct tax deductions and credits, homeownership provides long-term financial advantages.

Home equity can grow over time as mortgage balances decrease and property values rise. Combined with tax benefits such as deductions and credits, this makes homeownership an effective strategy for building long-term wealth.

According to federal guidance, deductions for mortgage interest and real estate taxes are among the most common tax benefits homeowners claim when filing their returns.

Homeownership in Massachusetts comes with several tax advantages that can help reduce the cost of owning a home. However, eligibility for these benefits often depends on factors such as income, filing status, and whether you itemize deductions. For the best results, homeowners should review current tax guidelines or consult a tax professional to ensure they maximize all available tax benefits.

Tip: If you’re looking for an affordable mortgage or want to check today’s mortgage rates in Massachusetts, you can explore the options available through Altgage. Comparing rates and loan programs can help you find a mortgage that fits your budget and long-term financial goals.

FAQs

1. Is Massachusetts a tax-friendly state for homeowners?

Massachusetts offers several tax benefits for homeowners, including deductions for mortgage interest, property taxes under federal rules, and state programs like the Senior Circuit Breaker Tax Credit.

2. Do Massachusetts homeowners qualify for property tax exemptions?

Yes. Many cities and towns in Massachusetts offer property tax exemptions for seniors, veterans, and individuals with disabilities. These exemptions are administered by local municipalities and may reduce the total property tax owed on a primary residence.

3. What is the Massachusetts Homestead Protection Act?

The Massachusetts Homestead Act allows homeowners to protect a portion of their home’s equity from creditors. Eligible homeowners can protect up to $500,000 in home equity by filing a Declaration of Homestead with the state.

4. Are there first-time homebuyer programs in Massachusetts?

Yes. Massachusetts offers several programs through the Massachusetts Housing Finance Agency (MassHousing) to help first-time buyers. These programs may include down payment assistance, affordable mortgage options, and homebuyer education resources.

5. Do Massachusetts homeowners get tax benefits for solar panels?

Yes. Massachusetts homeowners who install solar energy systems may qualify for federal clean energy tax credits and may also benefit from state programs like Solar Renewable Energy Certificates (SRECs) or other local incentives, depending on the installation.

6. Are home improvements tax-deductible in Massachusetts?

Most home improvements are not directly deductible, but improvements made for energy efficiency or renewable energy systems may qualify for federal tax credits. Additionally, certain improvements may increase the cost basis of the home, which can reduce capital gains tax when the property is sold.