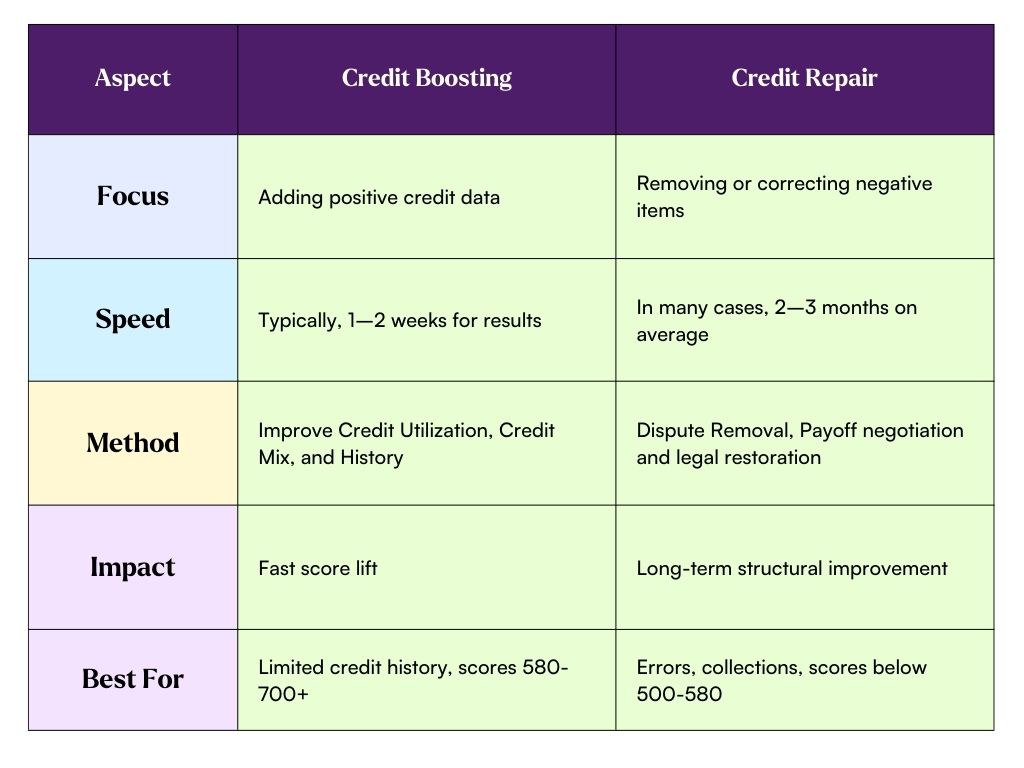

Two approaches. Different problems. Different timelines. Here's the difference in 30 seconds:

If you already know which one you need, jump to the section that fits. If you're not sure, keep reading — most borrowers preparing for a mortgage benefit from understanding both.

Credit Boosting: The 2-Week Path

Credit boosting is a set of strategies that add positive data to your credit report or speed up the reporting of accurate changes you've already made. It doesn't dispute anything. It doesn't try to remove negative marks. It works with what you have and optimizes it.

Strategies That Fall Under "Credit Boosting"

Rapid rescore (through a mortgage lender). The most powerful tool. You pay down a card, get a balance letter, and your lender submits it to the bureaus for a fast update. Score reflects the change in 3–14 days instead of 30–45. Read the full rapid rescore guide.

Utilization optimization. Paying credit cards below 10% of their limits is the fastest-acting score lever. Timing matters — pay before your statement closing date, not just the due date. Details in our guide on the 5 fastest ways to improve your score.

Authorized user strategy. Getting added to someone's well-managed credit card (high limit, low balance, long history, perfect payments) can add 15–40 points. Removing yourself from a harmful authorized user account can add 10–25 points.

Alternative data programs. Services like Experian Boost add utility payments, phone bills, and streaming subscriptions to your Experian report. These typically add 10–20 points to your Experian VantageScore — but be aware that most mortgage lenders use FICO models that don't incorporate this data. It's a good tool for non-mortgage applications, less reliable for mortgages. For why the models differ, see Mortgage Credit Score vs Consumer Credit Score.

Credit limit increases. Requesting a higher limit on existing cards (without adding a new card) lowers your utilization ratio without requiring you to pay anything down.

Who Credit Boosting Works Best For

- Score between 660 and 740 with room to optimize utilization

- Self-employed borrowers with high card balances from business expenses

- Borrowers with thin credit files who can benefit from authorized user additions

- Anyone within 20–80 points of a meaningful threshold (620, 680, 700, 740)

Who It Won't Help

- Borrowers with multiple recent late payments (last 12 months)

- Borrowers with active, unpaid collections

- Borrowers with a bankruptcy or foreclosure still reporting

- Anyone whose score is low due to factors that can't be rescored (short history, too many inquiries)

Credit Repair: The 6–12 Month Path

Credit repair focuses on removing inaccurate, outdated, or unverifiable negative items from your credit report. It's a dispute-driven process that works through the Fair Credit Reporting Act (FCRA), which requires credit bureaus to investigate and verify disputed items within 30 days.

How Credit Repair Works

Step 1: Pull your reports. Get your full credit reports from all three bureaus at AnnualCreditReport.com. Identify every negative item.

Step 2: Identify disputable items. Focus on items that are: inaccurate (wrong balance, wrong date, wrong status), not yours (mixed file, identity theft), outdated (should have aged off — most negatives drop after 7 years, bankruptcies after 10), or potentially unverifiable (small creditors who may not respond to bureau verification requests).

Step 3: File disputes. Submit disputes to each bureau — online, by mail, or through a credit repair agency. Each dispute triggers a 30-day investigation period.

Step 4: Repeat. Credit repair is iterative. Some items get removed on the first round. Others require multiple disputes. This is why it takes months.

DIY vs. Professional Credit Repair

DIY credit repair is free and effective if you're organized. You write the dispute letters, track responses, and follow up. The FCRA gives you the same rights as any agency.

Professional credit repair costs $50–$150/month and handles the process for you. The value is in experience — they know which disputes succeed, how to frame them, and when to escalate.

For mortgage-focused credit repair, Altgage partners with specialized providers who understand the scoring models lenders use and can prioritize the items most impacting your mortgage FICO. If you need a referral, ask your Altgage loan officer.

Important Distinction: Legitimate credit repair companies cannot guarantee specific score improvements or promise to remove accurate information. If a company guarantees results, that's a red flag. The FCRA only requires removal of items that are inaccurate, unverifiable, or outdated.

Who Credit Repair Works Best For

- Borrowers with errors on their report (duplicate accounts, wrong balances, accounts that aren't theirs)

- Borrowers with old collections (especially medical) that may be difficult for the creditor to verify

- Borrowers with a few isolated negative marks from 3+ years ago

- Anyone more than 12 months away from needing a mortgage

The Ideal Sequence: Both, in the Right Order

For most borrowers preparing for a mortgage, the question isn't "which one?" — it's "in what order?"

12 months before buying: Start credit repair if you have disputable negative items. File initial disputes with all three bureaus. Dispute in rounds, 30 days apart.

6 months before buying: Credit repair should be showing results. Begin DIY credit boosting — pay down utilization, audit authorized users. Pull reports again to assess progress.

2–4 weeks before applying: Final credit boosting push. Work with Altgage on a Rapid Credit Boost simulation. Execute the action plan (pay down remaining balances, get documentation). Rescore to lock in the final, optimized score.

Apply for mortgage: Score reflects both the long-term repair AND the short-term boost.

Why this order matters: Credit repair removes the anchors dragging your score down. Credit boosting maximizes the upside once those anchors are gone. Doing them in reverse (boosting first, then repairing) is less effective because the negative items cap how high the boosting strategies can push your score.

If you don't have 12 months: You can still benefit from credit boosting alone. Many borrowers see meaningful improvement just from utilization paydown and authorized user optimization — especially in the 660–730 range. Start with the 5 fastest ways to improve your score.

How to Know Which You Need

Are there errors or inaccurate items on your credit report?→ You need credit repair (or at minimum, bureau disputes).

Do you have old collections or negative marks from 3+ years ago?→ Credit repair may be able to remove them if the creditor can't verify.

Is your utilization above 30%?→ Credit boosting (utilization paydown) will have the biggest impact — potentially 30–60+ points.

Are you within 60 days of applying for a mortgage?→ Credit boosting and rapid rescore are your tools. Credit repair won't deliver results fast enough.

Is your score below 580?→ You likely need credit repair first. Boosting alone typically can't bridge that gap.

Is your score 660–740 with no major negative marks?→ Credit boosting alone may be all you need. This is the sweet spot for the Altgage Rapid Credit Boost.

Frequently Asked Questions

Can credit repair remove accurate late payments?

No — not legitimately. The FCRA only requires removal of information that is inaccurate, incomplete, or unverifiable. If you paid 30 days late and the creditor can verify it, the item stays. Any company claiming they can remove accurate negative marks is misrepresenting the process.

Is credit repair a scam?

Not inherently — but the industry has bad actors. Legitimate companies charge monthly fees (not large upfront payments), don't guarantee specific point improvements, and don't advise illegal tactics. The FTC and CFPB have enforcement records against fraudulent companies.

How long do negative items stay on my credit report?

Most negative items (late payments, collections, charge-offs): 7 years from the date of first delinquency. Bankruptcies: 7 years (Chapter 13) or 10 years (Chapter 7). Hard inquiries: 2 years (but only impact your score for about 12 months).

Can I do credit repair and a rapid rescore at the same time?

Yes — the ideal sequence does exactly this. Address long-term items through credit repair over months, then use a rapid rescore in the final weeks to optimize the remaining short-term factors.

What's Experian Boost? Is that credit boosting?

Yes, but with a major caveat: Experian Boost adds utility, phone, and streaming payments to your Experian report and improves your VantageScore. Most mortgage lenders use FICO models that don't incorporate this data. Useful for non-mortgage credit but unreliable for mortgage preparation.

The Bottom Line

Credit boosting and credit repair aren't competing strategies — they're complementary. Repair clears the debris. Boosting maximizes the score. The best results come from using both in the right sequence, timed to your mortgage application.

If your mortgage is 6+ months away and you have negative marks, start credit repair now. If you're ready to buy soon and your score just needs optimization, Altgage's Rapid Credit Boost can deliver 20–100 points in about two weeks — free, with an 80%+ success rate.

Either way, start by seeing where you actually stand. Check live rates at rates.altgage.com, or get pre-approved.

Related Reading on Altgage

- How to Boost Your Credit Score for a Mortgage (Fast)

- What Is a Rapid Rescore? Can I Do It Myself?

- How Much Does a Rapid Rescore Improve Credit?

- 5 Fastest Ways to Boost Your Credit Score Before a Mortgage

- How Much Is PMI?

- Why Is My Credit Score Different on Different Sites?

- See Your Rate →

- Get Pre-Approved →