.avif)

Your banking app says 718. Your mortgage lender says 682. That 36-point gap isn't a glitch — it's the difference between the consumer credit score you see online and the mortgage-specific FICO score lenders actually use. And it's probably costing you money.

A rapid rescore is the fastest way to close that gap. But there's a catch: you can't do it yourself.

What a Rapid Rescore Actually Does

When you pay off a credit card or fix an error on your report, that change doesn't show up immediately. Credit card issuers report to the bureaus once per billing cycle — roughly every 30 days. That means even if you paid your card to $0 today, your credit report (and score) won't reflect it for up to 45 days.

A rapid rescore bypasses that wait. Your mortgage lender submits proof of the change — a balance letter, a paid-in-full statement, a corrected account record — directly to the credit bureaus, and your report is updated in 3–5 business days.

That's it. No magic, no hacking, no loophole. It's just fast-tracking the reporting of accurate, already-completed changes.

What a Rapid Rescore Is NOT

This distinction matters, because borrowers confuse these constantly:

It's not credit repair. Credit repair disputes negative items — late payments, collections, charge-offs — and tries to get them removed. That process takes 3–12 months and works only on items that are inaccurate or unverifiable. A rapid rescore doesn't dispute anything. For a full comparison, read Credit Boosting vs. Credit Repair.

It's not a credit hack. You can't rescore your way out of legitimate problems. If you have four late payments and a bankruptcy, a rescore won't help. The underlying changes have to already exist — the rescore just makes sure the bureaus know about them faster.

It's not a score guarantee. The rescore updates your report. If the updated information is positive (lower balance, corrected error), your score will likely improve. But credit scoring is complex, and the exact point change depends on your full profile.

Can I Do a Rapid Rescore Myself?

No. This is the single most common question we get, and the answer is definitive.

A rapid rescore can only be initiated by a credentialed mortgage lender or broker who has a direct relationship with the credit bureaus' rapid rescore system. There is no consumer portal. There's no app. There's no website where you can submit your own documentation and get an expedited update.

The reason: the rapid rescore system exists specifically within the mortgage origination workflow. It's designed for situations where a borrower is actively applying for a mortgage and a score update could change their loan terms. The credit bureaus don't offer this service to individuals.

What you CAN do on your own:

- Dispute errors through the standard process at each bureau's website (takes 30–45 days)

- Pay down balances and wait for the next billing cycle to report (30 days)

- Use services like Experian Boost to add utility/phone payments (limited impact, VantageScore only — doesn't affect mortgage FICO)

If you want to start improving on your own right now, read 5 Fastest Ways to Boost Your Credit Score Before a Mortgage. But if timing is tight — and in a mortgage application, it almost always is — the lender-initiated rescore is the path.

When Does a Rapid Rescore Make Sense?

A rescore is valuable when you're close to a threshold that changes your loan terms:

Crossing 740 for conventional loans. Above 740, you get the best available rates and the lowest PMI. A borrower at 720 who rescores to 745 can save $165+ per month on a $350,000 loan.

Reaching 620 for conventional eligibility. Below 620, you're limited to FHA (which requires 580+). If you're at 610 and a paid-off card would push you to 625, a rescore gets you into conventional loan territory.

Qualifying for a DSCR loan. Most DSCR lenders want 660+, and better scores mean lower down payments and rates. A rescore from 650 to 680 can unlock the product entirely.

Correcting an error before rate lock. If an error is dragging your score down and you've already submitted a dispute but can't wait 30–45 days, a rescore with documentation of the correction updates your file immediately.

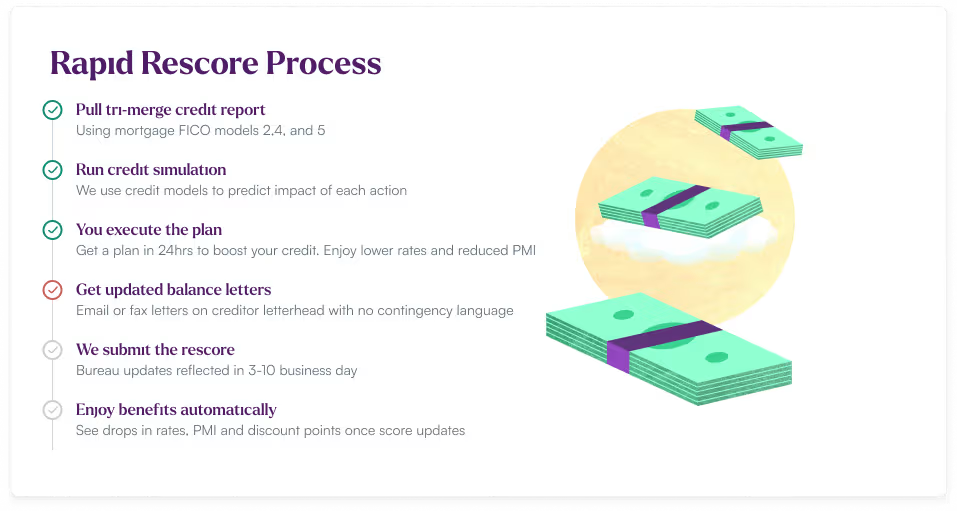

The Rapid Rescore Process

Here's what happens when you work with Altgage:

1. We pull your tri-merge report. All three bureaus, using mortgage FICO models (2, 4, and 5). This shows us exactly where you stand and identifies the opportunities. For more on why your mortgage score differs from your app score, read Mortgage Credit Score vs Consumer Credit Score.

2. We run a simulation. A credit expert models specific actions — paying down Card A, removing Authorized User B, correcting Error C — and projects the point impact of each.

3. You execute the action plan. Pay the balances, get the documentation, make the authorized user changes. We guide you through the process.

4. You provide documentation. Balance letters on creditor letterhead, payment confirmations, corrected account statements. No contingency clauses, no conditional language.

5. We submit for rescore. The documentation goes to the bureaus through our direct channel, and your updated score comes back in 3–14 business days.

One important limitation: you typically get one rescore per file. That's why the simulation matters — we need to bundle every improvement into a single submission.

What Does a Rapid Rescore Cost?

At Altgage, the Rapid Credit Boost (our rescore program) is free — included as part of our mortgage preparation process.

Not all lenders do this. Some charge $25–$50 per tradeline per bureau — so if you're rescoring three accounts across three bureaus, that could be $225–$450. Ask about cost upfront before starting the process with any lender.

How Much Will a Rapid Rescore Improve My Score?

The typical range is 20–100 points, with an 80%+ success rate:

SituationTypical ImprovementPaying down high utilization (50%+ → under 10%)40–80 pointsAdding a strong authorized user account15–30 pointsRemoving a harmful authorized user10–25 pointsCorrecting a balance error20–50 pointsPaying off a collection15–40 pointsAlready low utilization, clean file0–15 points

For detailed improvement scenarios by profile type, read How Much Does a Rapid Rescore Improve Credit?

Frequently Asked Questions

How long does a rapid rescore take?

3–14 business days from documentation submission. Most updates come back within one week. The bottleneck is usually getting balance letters from creditors, not the rescore itself.

Will a rapid rescore show up as a hard inquiry?

No. The rescore itself is not a credit pull — it's an update to existing data. However, the initial tri-merge credit pull that starts the process is a hard inquiry (typically 2–5 points, and it's required for any mortgage preapproval).

Can a rapid rescore lower my score?

Only if the updated data is negative — for example, if a balance increased. That's why we run the simulation first and only proceed when the projected outcome is positive.

Does a rapid rescore work for FHA loans?

Yes. While FHA has flat mortgage insurance (0.55% regardless of score), your credit score still affects your interest rate and whether you qualify at all (580 minimum for 3.5% down). A rescore can help borrowers clear the 580 or 620 thresholds.

Can I get multiple rescores?

Typically one per file per application. Some lenders allow a second in limited circumstances, but the standard practice is to bundle all improvements into a single rescore.

The Bottom Line

A rapid rescore is the fastest legitimate way to improve your mortgage credit score — turning 30–45 days of waiting into 3–14 days of action. It can't fix everything, but for borrowers with fixable issues (high utilization, outdated balances, errors, authorized user problems), it's the difference between getting the rate you want and settling for less.

You can't do it yourself. You need a mortgage lender who offers the service. At Altgage, the Rapid Credit Boost is free, it takes about two weeks, and it has an 80%+ success rate. Check live rates at rates.altgage.com, or get pre-approved.