You're buying a home with less than 20% down, and your lender mentions private mortgage insurance (PMI). Your first question: how much is this actually going to cost me?

The answer ranges from $26 to $534 per month on a $400,000 home — and the biggest factor isn't what most people think. It's not your down payment. It's your credit score, by a factor of roughly 7x. Use the calculator below to see your number in seconds, then keep reading for the full picture.

PMI Calculator

Enter your home price, down payment, and credit score range to see your estimated monthly PMI cost. The calculator uses actual MGIC/Radian rate card data and shows you how much you could save by improving your credit score.

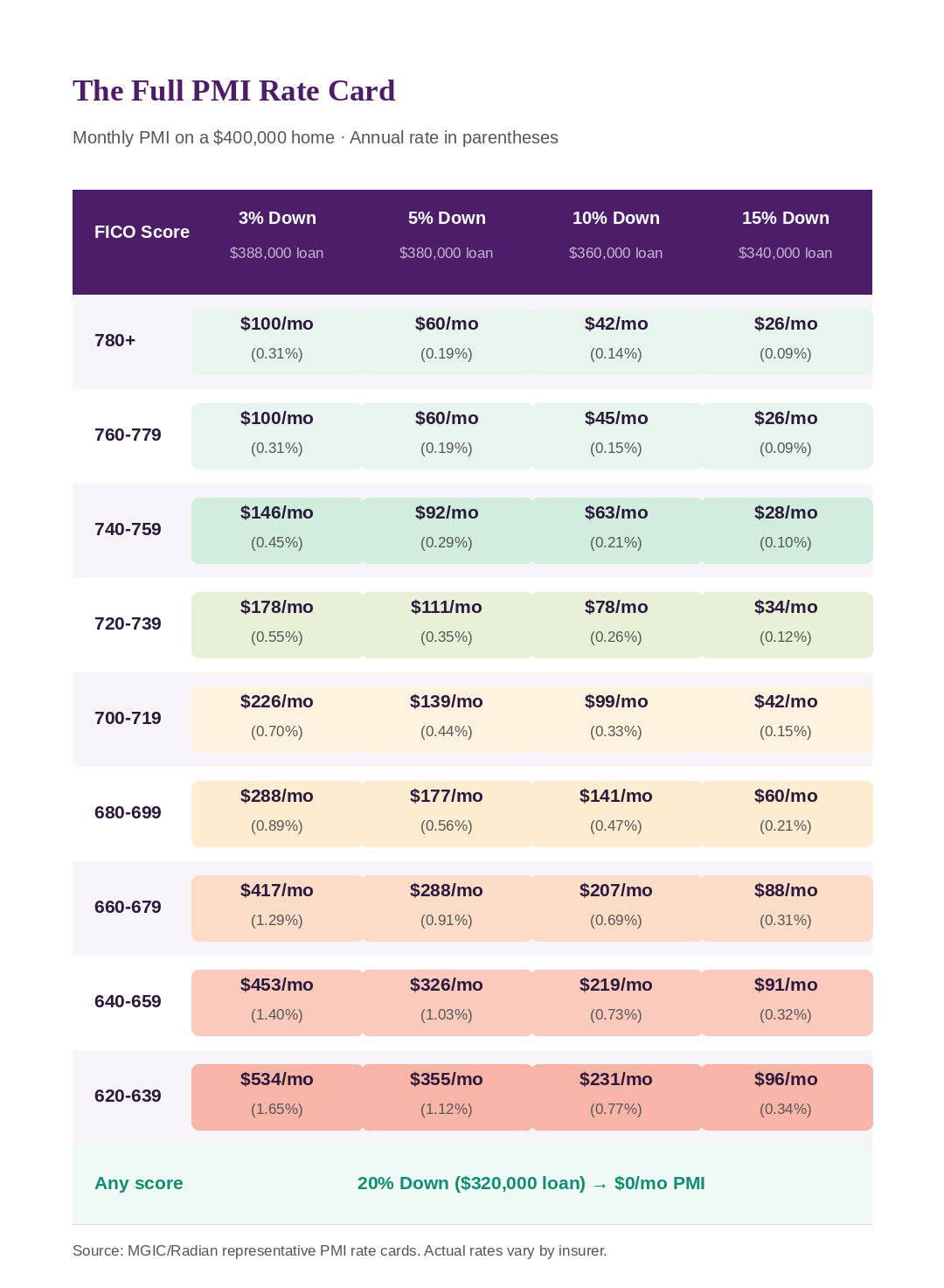

PMI is priced by two main factors: your credit score (FICO) and your loan-to-value ratio (LTV), which is 1- down payment %. The higher your score and the larger your down payment, the less PMI costs. Most buyers assume down payment is the primary driver. It's not. Your credit score has a dramatically larger impact on your monthly PMI payment. The rate card below shows exactly how much. PMI is quoted as an annual percentage of your loan amount, then divided by 12 for your monthly payment. A rate of 0.35% on a $380,000 loan means $380,000 × 0.0035 ÷ 12 = $111 per month.

PMI Rate Cards - Credit vs Down Payment

Here's what mortgage insurers actually charge. This table shows annual PMI rates as a percentage of your loan amount, broken down by FICO score and down payment size:

Notice how the top-right corner (high credit, higher down payment) is nearly free — 0.09% annually, or about $26/month on a $340,000 loan. The bottom-left corner (low credit, minimal down payment) is 1.65%, or about $534/month on a $388,000 loan. That's a 20x difference driven almost entirely by credit score.

How much is PMI on a $400,000 home?

Percentages are useful, but you want the actual dollar amount. Here's what PMI costs on a $400,000 home at several common scenarios:

With 5% down ($380,000 loan):

- 620–639 credit score: $380,000 × 1.12% ÷ 12 = $355/month

- 680–699 credit score: $380,000 × 0.56% ÷ 12 = $177/month (that's 50% less)

With 10% down ($360,000 loan):

- 680–699: $141/month

- 720–739: $78/month (another nearly 50% cut)

With 15% down ($340,000 loan):

- 720–739: $34/month

- 760+: $26/month

The range is enormous. Credit improvements in the lower tiers can see a dramatic reduction in costs. Increasing down payments or already good credit scores see marginal improvments, albeit boosting credit is still the most efficent. On the exact same $400,000 home, PMI costs anywhere from $26/month (780+ score, 15% down) to $534/month (620 score, 3% down). That's a 20x difference.

Credit Score Matters 7x More

This is the insight that changes how you think about PMI. Compare the two levers side by side on a $400,000 home:

The credit score lever (holding down payment at 5%):Improving from 620 to 760+ saves $295 per month in PMI ($355 → $60). Cost to you: $2-$5K in additional cash to pay-off debt and reduce credit utilization.

The down payment lever (holding credit score at 760+):Increasing from 5% to 15% saves $34 per month in PMI ($60 → $26). Cost to you: an additional $40,000 in cash.

The credit score improvement saves 8.7x more per month ($295/$34) than tripling your down payment — and requires limited savings. Even a moderate improvement from 680 to 740 at 5% down saves $85/month ($177 → $92), while saving an extra $20,000 for 10% down at the same 680 score only saves $36/month ($177 → $141). Before saving another dollar toward a bigger down payment, check whether a 40–60 point credit score improvement could cut your PMI cost in half. Altgage offers a complimenatry rapid rescore service to help you save. Apply here →

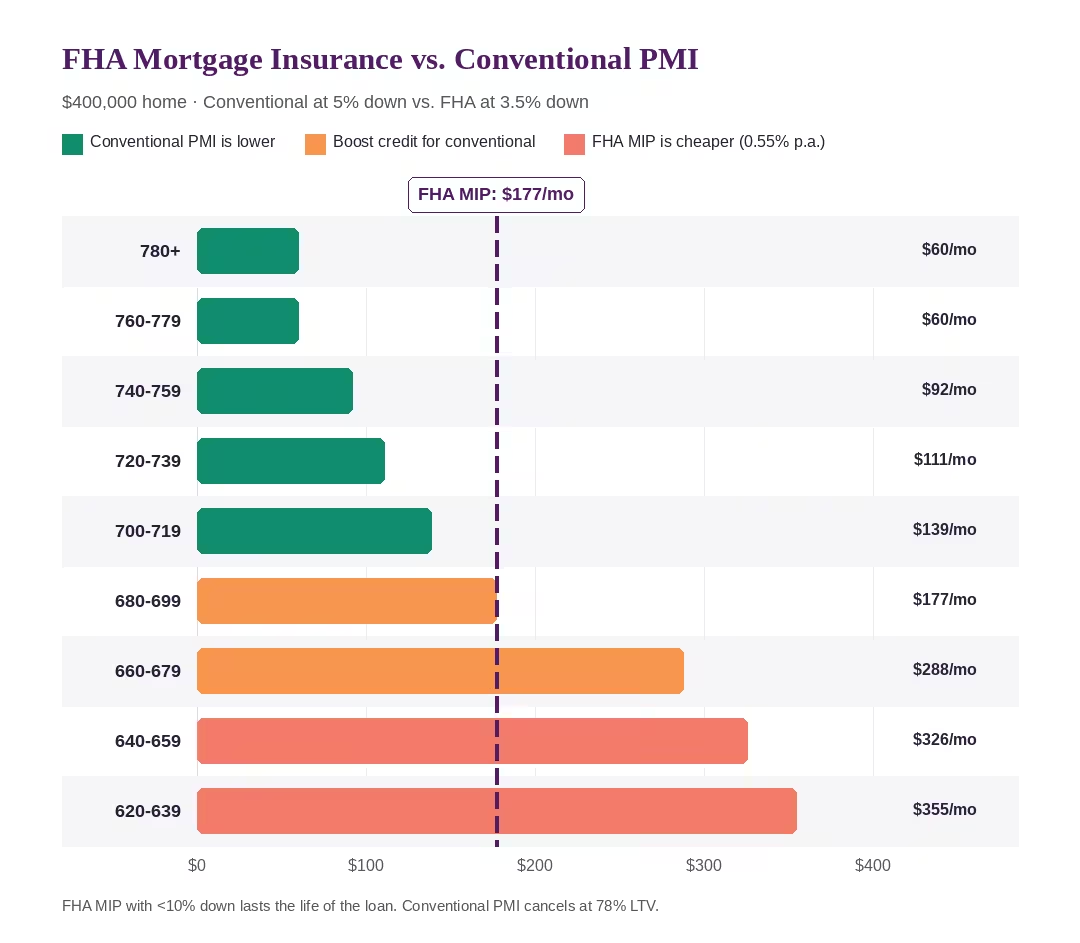

Conventional PMI vs. FHA Mortgage Insurance

If your credit score is below 680, your loan officer has probably mentioned FHA as an option — and for good reason. FHA loans charge a flat 0.55% annual mortgage insurance premium (MIP) regardless of your credit score. On a $400,000 home with 3.5% down ($386,000 loan), that's $177/month. Compare that to conventional PMI at 5% down on the same home: a borrower with a 660 score pays $288/month in PMI, while a 620 score borrower pays $355/month. FHA's flat $177 beats both of those by a wide margin. But the crossover happens at 680 FICO. Above 680, conventional PMI drops below FHA MIP — and the gap widens fast. At 740+, conventional PMI is roughly half the cost of FHA. At 780+, it's roughly a third.

The monthly payment is only half the story. There are two structural differences that make conventional the stronger long-term choice when your score qualifies:

FHA MIP is permanent. On FHA loans with less than 10% down, MIP stays for the life of the loan. It never cancels. The only way to eliminate it is to refinance into a conventional loan once you have enough equity — which means paying closing costs again. Conventional PMI, by contrast, cancels automatically at 78% LTV.

FHA charges upfront MIP too. FHA adds a 1.75% upfront mortgage insurance premium ($6,755 on a $386,000 loan), typically rolled into the loan balance. This increases your total loan amount and the interest you pay over the life of the mortgage. Conventional loans have no equivalent upfront charge.

What if your loan exceeds the FHA limit? FHA loan limits vary by county — in 2026, the standard floor is $541,287 and the high-cost ceiling is $1,249,125. If the home you're buying pushes your loan above the FHA limit for your area, conventional is your only option. In that scenario, a credit score boost before closing isn't just helpful — it's the primary lever you have to control your PMI cost. A rapid rescore that moves you from 660 to 720 saves $177/month in PMI on a $380,000 loan. Read our guide to rapid rescoring →

We evaluate FHA with flat MIP versus conventional with score-based PMI for every borrower, factoring in the upfront MIP, the cancellation timeline, and total cost over the life of the loan. Sometimes FHA wins by $200/month. Other times FHA wins by $50/month but costs you $15,000 more over the life of the loan.

The Bottom Line

PMI costs anywhere from negligible to significant — and the single biggest factor is your credit score, not your down payment. A buyer with a 760+ score and 5% down pays just $60/month on a $400,000 home. A 620-score buyer at the same down payment pays nearly $355/month. If your PMI quote seems high, shop rates across lenders and boost your credit score. A 40–60 point improvement through rapid rescoring can cut your PMI cost in half, saving you far more per month than an extra $20,000–$40,000 in down payment. PMI is the cheapest ticket to homeownership, so don't' wait to save 20% down. There's also several ways to cancel PMI

For buyers with 680+ credit, conventional PMI beats FHA mortgage insurance on both monthly cost and long-term cost — and it cancels automatically. For buyers below 680, FHA's flat 0.55% rate is usually the better monthly deal, but remember: it's permanent unless you refinance.

Check your rate at Altgage to see your personalized PMI estimate, compare FHA vs. conventional side by side, and find out how much a credit score boost could save you.

Frequently Asked Questions

How much is PMI on a $300,000 house?

With 5% down ($285,000 loan) and a 720–739 credit score, PMI is approximately $83/month (0.35% annual rate). With a 760+ score, it drops to about $45/month. A 620-score borrower at the same down payment pays roughly $266/month.

How much is PMI per month?

PMI ranges from about $26 to over $500 per month, depending on your credit score, down payment, and loan amount. On a $400,000 home with 5% down, monthly PMI runs from $60 (760+ score) to $355 (620 score). Most buyers with good credit (700+) pay between $45 and $140 per month.

Is PMI based on credit score or down payment?

Both, but credit score has roughly 7x more impact. Improving from 680 to 740 typically saves more per month than increasing your down payment from 5% to 15% — and a credit score improvement costs $0 in additional savings. See the full rate card above for the exact numbers.

How much is PMI on an FHA loan?

FHA loans charge a flat 0.55% annual MIP regardless of credit score, plus a 1.75% upfront premium. On a $400,000 home with 3.5% down, that's $177/month — cheaper than conventional PMI for scores below 680, but more expensive for higher scores. And unlike conventional PMI, FHA MIP with less than 10% down never cancels.

How much is PMI in Texas?

PMI rates are national — they don't vary by state. Your PMI cost in Texas is determined by the same credit score and LTV factors as anywhere else. However, Texas home prices affect your loan amount, which determines the dollar amount. Use our calculator above with your specific home price.

Can I avoid PMI without putting 20% down?

Yes. Options include lender-paid mortgage insurance (LPMI), piggyback loans (80-10-10), VA loans (no PMI), and professional/physician loans. Each has trade-offs. Read our complete guide to avoiding PMI →

Does PMI ever go away?

On conventional loans, PMI automatically cancels at 78% LTV and you can request removal at 80% LTV. FHA mortgage insurance with less than 10% down stays for the life of the loan — refinancing into a conventional loan is the only exit. Read our guide on when PMI goes away →

How is PMI calculated?

PMI is an annual percentage of your loan amount, divided by 12 for your monthly payment. The percentage comes from the mortgage insurer's rate card, which prices based on your FICO score and LTV ratio. For example: $380,000 loan × 0.35% annual rate ÷ 12 = $111/month.

Related Reading on Altgage