You want to get pre-approved for a mortgage, but you're nervous. You've heard that applying for credit hurts your score, and the last thing you need right before buying a home is a credit score drop.

Here's the good news: the impact is smaller than most people think, and the credit scoring system is specifically designed to let you shop for mortgage rates without being penalized. Let's break down exactly what happens to your credit when you get pre-approved.

Your credit score exists to help you access life's most important financial milestones. There is nothing more meaningful than having a home to raise a family in. Worrying about a temporary 3–5 point dip — while paying $1,800/month in rent that builds zero equity — is like skipping the gym because you're worried about sore muscles. The cost of inaction is far greater than the cost of a credit inquiry.

When Does the Score Drop Happen?

First, a common misconception: your score doesn't drop when you check it. It drops the moment the lender pulls your credit. If a lender runs a hard pull on Monday morning, your score reflects that inquiry immediately — even if you don't look at your own score until Friday. Checking your own credit (through Credit Karma, annualcreditreport.com, or your bank's free score tool) is always a soft pull with zero impact.

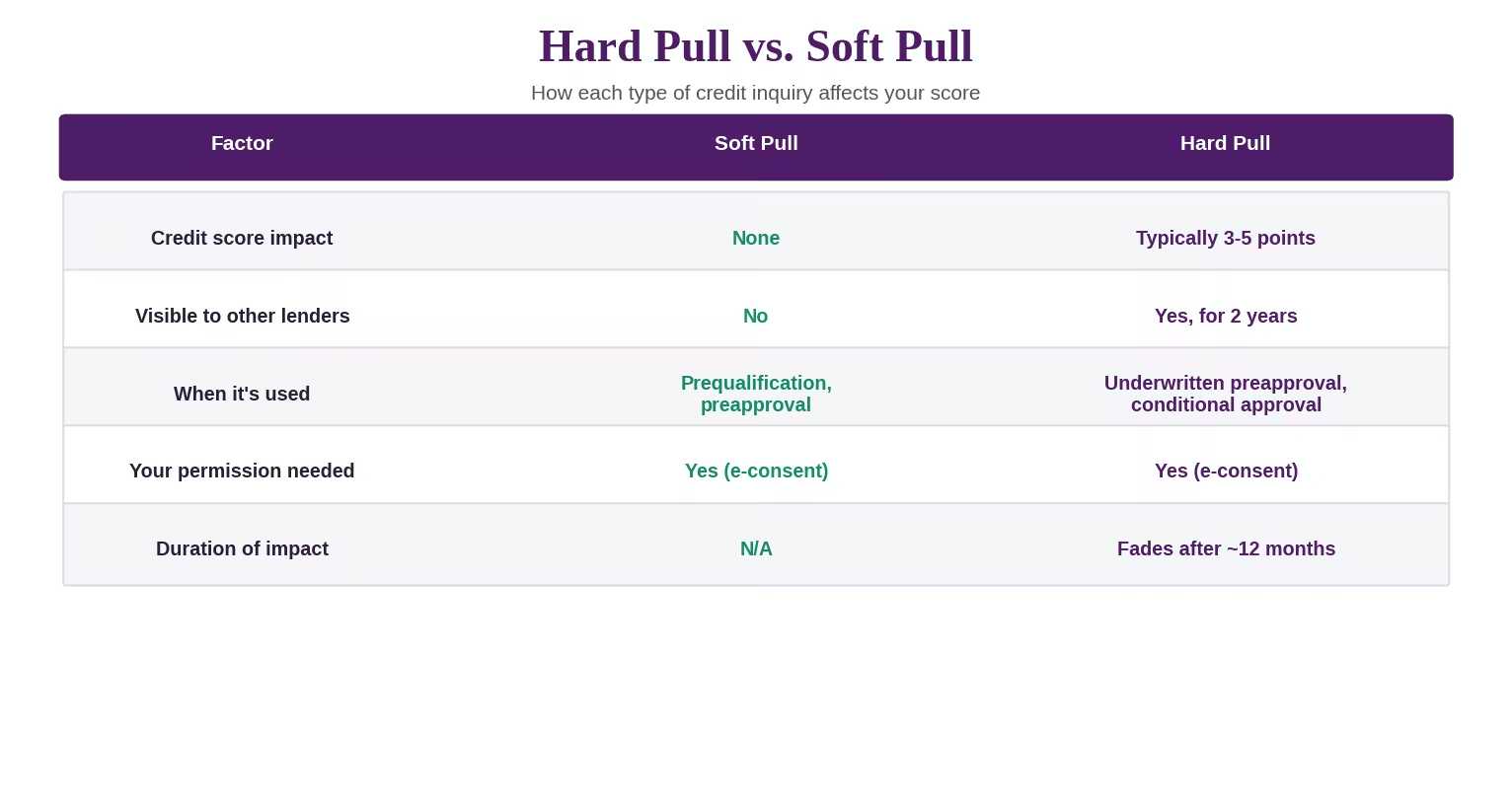

Hard Pull vs. Soft Pull: What's the Difference?

Not all credit checks are created equal. There are two types, and they affect your score very differently:

Soft Pulls

A soft pull checks your credit report without affecting your score. Soft pulls are used for prequalification and preapproval — when a lender verifies your financial picture and gives you a rate estimate. At Altgage, both our prequalification and preapproval use soft pulls, so you get an accurate picture of your rate eligibility without any credit score impact.

Hard Pulls

A hard pull is a formal credit inquiry that pulls your full tri-merge credit report (Equifax, Experian, TransUnion). This typically happens with underwritten preapprovals — especially for VA and FHA loans — and always occurs during conditional approval when a property is under contract.

A single hard pull typically lowers your score by 3 to 5 points. For most borrowers, this is negligible — and frankly, it's a small price to pay for the most important purchase of your life.

The 45-Day Rate Shopping Window

Here's the rule that most homebuyers don't know about: all mortgage inquiries within a 45-day window are counted as a single hard pull for FICO scoring purposes.

This means you can apply with five different lenders in the same month, each one pulling your credit, and your FICO score treats it as one inquiry. The scoring model recognizes that you're shopping for the best rate on a single mortgage — not applying for five different loans.

The 45-day window applies to FICO scoring models (used by most mortgage lenders). VantageScore uses a 14-day window. Since most mortgage lenders use FICO, the 45-day window applies to the vast majority of mortgage applications. To be safe, do your comparison shopping within 14 days.

This is why rate shopping is so important. You have a full 45-day window to compare lenders with essentially zero additional credit impact. Not shopping means you're leaving money on the table.

How Much Will a Mortgage Inquiry Actually Affect Your Score?

Let's put this in perspective with real numbers:

For the vast majority of borrowers, a mortgage inquiry has zero practical effect on their rate or approval. The only time it matters is when you're right at a scoring threshold — and even then, the effect is temporary and often fixable with rapid rescoring.

Forget the 3-Point Drop — Use the Hard Pull to Boost Your Score

Here's what most articles about credit inquiries won't tell you: a hard pull is actually an opportunity, not a setback.

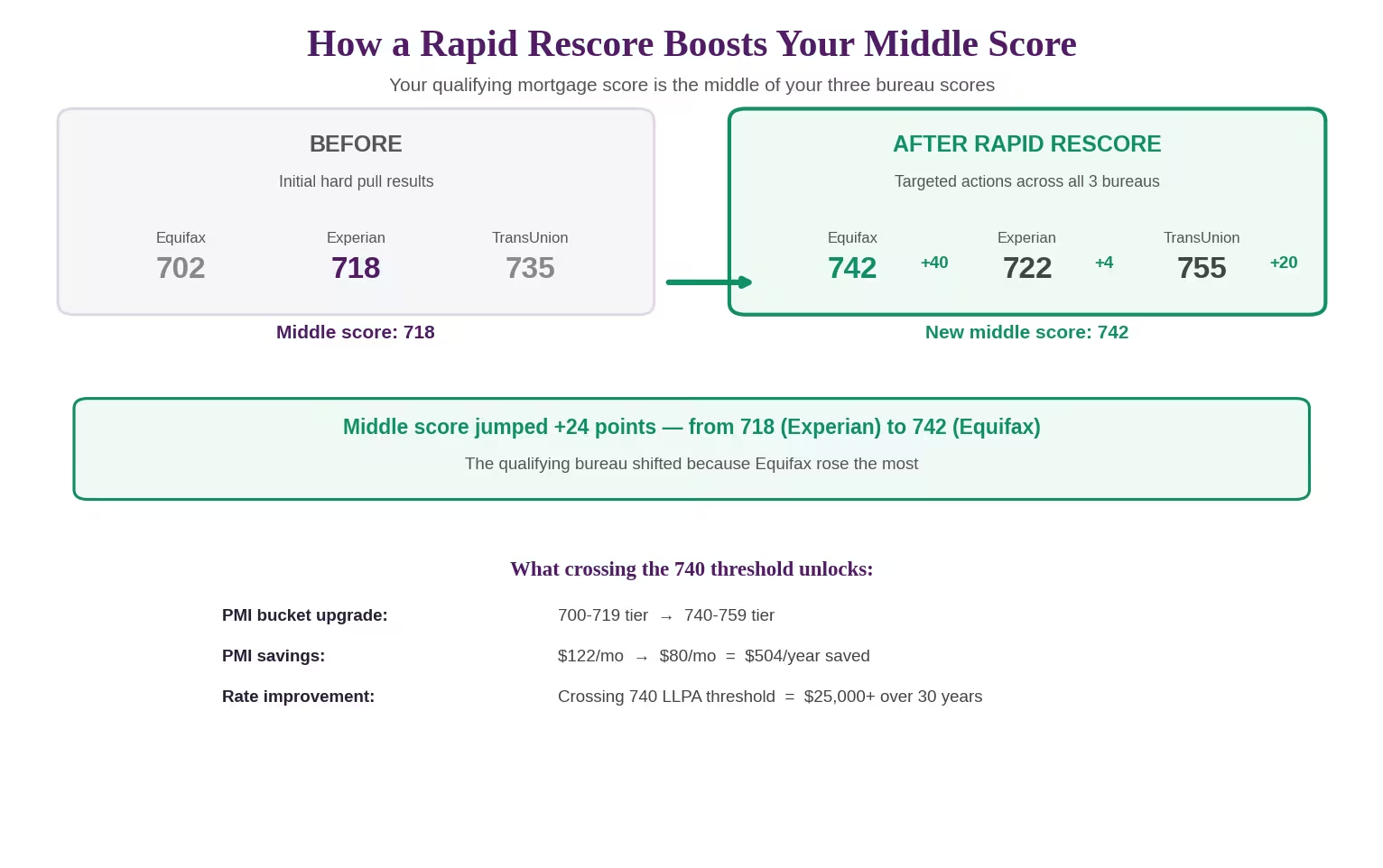

When a lender runs a hard pull, they pull your full tri-merge credit report from all three bureaus — Equifax, Experian, and TransUnion. Your qualifying mortgage score is the middle score across the three. This is the first time you and your lender see the exact number that determines your rate and PMI pricing.

At Altgage, once we have that middle score, our team runs a rapid rescore simulation to figure out how to move all three bureau scores in tandem — so the new middle score lands higher than where you started. Instead of worrying about a 3–5 point inquiry drop, borrowers working with Altgage frequently boost their score by 20–60 points through targeted actions like paying down specific credit card balances, correcting reporting errors, or optimizing utilization ratios.

The savings from even a modest score improvement are massive — and they compound across both your interest rate and your PMI:

PMI savings from a credit score boost ($350,000 home, 5% down):

- Moving from 700-719 to 740-759: PMI drops from $122/mo to $80/mo — that's $42/month or $504/year in savings

- Moving from 720-739 to 760+: PMI drops from $97/mo to $53/mo — that's $44/month or $528/year in savings

And that's just PMI. Crossing the 740 FICO threshold also improves your Loan Level Pricing Adjustments (LLPAs) — the behind-the-scenes pricing that directly affects your mortgage rate. A 24-point improvement that crosses 740 can save $25,000+ over the life of a 30-year loan.

Altgage Perspective: The hard pull isn't the end of the story — it's the starting line. Once we see your tri-merge scores, we run a simulation to identify the fastest path to a higher middle score. In the example above, a borrower starting at 718 crossed the critical 740 threshold after rescore — unlocking better PMI pricing and LLPA savings worth thousands per year. Read our full rapid rescoring guide for the step-by-step strategy.

Prequalification vs. Preapproval: What's Actually Different?

These terms get confused constantly, and even some lenders use them loosely. Here's what they actually mean:

Prequalification (Soft Pull)

- Quick estimate based on self-reported income, assets, and debts

- Soft credit check — no score impact

- No document verification — the lender takes your word for it

- Not a commitment from the lender

- Useful for: understanding your budget range early in the process

Preapproval (Soft Pull)

- Lender verifies your documents — pay stubs, bank statements, tax returns

- Soft credit check in most cases (including at Altgage)

- Results in a preapproval letter — a conditional indication of what you qualify for

- Much stronger than prequalification because financials are verified, not self-reported

- Useful for: making competitive offers, knowing exactly what you qualify for

The key difference: prequalification uses self-reported numbers, preapproval verifies them. Both typically use soft pulls, so neither hurts your score.

Altgage's Approach: Start with a free quote (no credit pull required) at rates.altgage.com to see where you stand. When you're ready to make offers, we'll move to full preapproval with document verification — still a soft pull. You only encounter a hard pull if you need an underwritten preapproval for VA/FHA, need a rapid rescore, or when you go under contract.

Tips to Minimize Credit Score Impact

- Start with preapproval. Get your rate estimate and budget range through a soft pull before committing to anything more.

- Do all your rate shopping within a 14-day window. While FICO gives you 45 days, VantageScore uses 14 days. Playing it safe with a tighter window covers both models.

- Avoid other credit applications. Don't apply for credit cards, auto loans, or any other credit products during your mortgage process. Each of those is a separate hard inquiry that doesn't get the mortgage shopping protection.

- Check your own credit first. Pull your own reports at annualcreditreport.com (free, no score impact) to catch errors before a lender does.

- Don't open new accounts. New accounts lower your average account age and can raise red flags during underwriting.

Frequently Asked Questions

How long does a hard inquiry stay on my credit report?

Hard inquiries remain on your report for 2 years but only affect your FICO score for approximately 12 months. After 12 months, the inquiry is still visible but has zero scoring impact.

Can I get preapproved without a hard pull?

Yes — most lenders, including Altgage, offer preapproval with a soft pull. The soft pull gives lenders enough information to verify your rate eligibility and issue a preapproval letter. A hard pull (tri-merge credit report) is typically only required for underwritten preapprovals on VA/FHA loans or when you go under contract on a property.

Will multiple preapprovals hurt my score?

Not if they're within the 45-day FICO shopping window. Five preapprovals in one month = one inquiry's worth of impact (3–5 points). This is specifically designed to encourage rate shopping.

Should I get preapproved before looking at homes?

Yes. Preapproval tells you exactly how much you can borrow, what rate you'll get, and makes your offers more competitive. Most listing agents won't take an offer seriously without a preapproval letter. Start with a soft-pull prequalification at rates.altgage.com to see where you stand, then move to full preapproval when you're ready to shop.

What if my score drops below a key threshold after the inquiry?

If a mortgage inquiry pushes you just below a threshold (say, from 620 to 615), talk to your loan officer about rapid rescoring. In some cases, quick actions like paying down a credit card balance can boost your score within days.

The Bottom Line

Getting preapproved for a mortgage will have a minimal, temporary impact on your credit score — 3 to 5 points that fades within 12 months. The 45-day shopping window means you can compare multiple lenders without compounding the impact.

Don't let credit score anxiety stop you from getting preapproved. The information you gain — your actual rate, loan amount, and monthly payment — is far more valuable than the 3–5 points you'll temporarily lose. And with a lender like Altgage who runs rapid rescore simulations after the hard pull, that inquiry can actually become the catalyst for a 20–60 point increase that saves you thousands in PMI and interest. Credit exists to help you build a life. Use it.

Related Reading on Altgage

- What Is a Rapid Rescore?

- Should I Lock My Mortgage Rate Today?

- How to Avoid PMI on Your Mortgage

- Get Your Rate (No Credit Needed)