You've saved diligently for a down payment, found a home you love, and then your lender drops the news: because you're putting down less than 20%, you'll need to pay private mortgage insurance (PMI). On a $400,000 home, that's an extra $63 to $335 per month — depending almost entirely on one thing most buyers overlook. PMI exists to protect the lender if you default, not to protect you. So naturally, most homebuyers want to know: is there a way around it?

The answer is yes — several ways, in fact. But before you make avoiding PMI your top priority, you need to understand what actually drives PMI cost — and why delaying homeownership to dodge it may be the most expensive decision you make.

Is PMI expensive?

PMI vs down payment at a 720 credit score

With a 720 credit score and 5% down, PMI is $111/mo. At 15% down it's $34/mo. The entire down payment swing from 5% to 15% saves just $77/month — and costs you an extra $40,000 in cash. The credit score swing from 620 to 760+ at the same down payment saves $295/month. Before saving another dollar for a down payment, boosting your credit score by 40–60 points can cut your PMI cost in half. Read our guide to rapid rescoring to see how fast you can move the needle.

5 Strategies to avoid PMI

Not every buyer should embrace PMI. If your credit score is below 680 and FHA loans are not an option because of the loan amount, PMI costs climb steeply and the math shifts. Here are five ways to avoid it — and when each one makes sense.

Strategy 1: Put 20% Down

The most straightforward way. On a $400,000 home, that's $80,000. Works best for buyers selling a previous home or receiving a large gift. Just make sure the opportunity cost of tying up that cash is worth the PMI savings.

Strategy 2: Lender-Paid Mortgage Insurance (LPMI)

The lender covers PMI in exchange for a 0.125%–0.375% higher rate. No separate PMI payment, but you can't cancel it — the higher rate stays unless you refinance. Best for 5–7 year holds where the break-even math favors a slightly higher rate over monthly PMI.

Strategy 3: Piggyback Loan (80-10-10)

Two loans: 80% first mortgage (no PMI), 10% second mortgage, 10% down. Combined payment is often less than single mortgage + PMI, but adds two-loan complexity and the second mortgage usually carries a variable rate.

Strategy 4: VA or USDA Loan

VA and USDA loans never require PMI with 0 money down. If you're eligible, these are almost always the best path — VA loans in particular offer competitive rates with zero down and no ongoing mortgage insurance. FHA loans don't charge PMI — but they do charge their own mortgage insurance (MIP) which works differently. Whether FHA or conventional mortgage insurance costs you less depends on your credit score and the PMI crossover. See PMI vs. MIP: Which costs more? →

Strategy 5: Professional or Jumbo Loans

Some lenders waive PMI for doctors, attorneys, CPAs, and other professionals — even with low down payments. These "physician loans" or "professional mortgages" recognize high future earning potential and in many cases are similar to Jumbo loans without the PMI or 20% down payment requirement.

PMI Is the golden ticket to homeownership

The internet is full of advice about how to avoid PMI. But here's what those articles rarely say: for buyers with good credit, PMI may be the cheapest ticket to homeownership you'll ever get. At a 780+ score with 5% down, your PMI is $60/month. That's less than take out. And it's temporary — PMI cancels automatically once you reach 78% LTV through regular payments and appreciation. You can cancel it even earlier. Here are 6 strategies to remove PMI.

Consider the real cost of waiting to save 20% down to avoid that $60/month:

- Home price appreciation: Home prices have averaged 3–5% annual appreciation in most markets. That's $12,000–$20,000/year on a $400,000 home — money you either capture as equity or lose while renting.

- Rent payments: At $2,000/month, that's $24,000/year building zero equity while you save for that bigger down payment.

- PMI is temporary: On conventional loans, PMI cancels at 78% LTV. Most buyers eliminate it in 5–8 years through a combination of regular payments and home appreciation.

- PMI is small relative to total payment: At $60/mo, PMI is roughly 2.5% of your total PITI payment. You probably spend more on coffee.

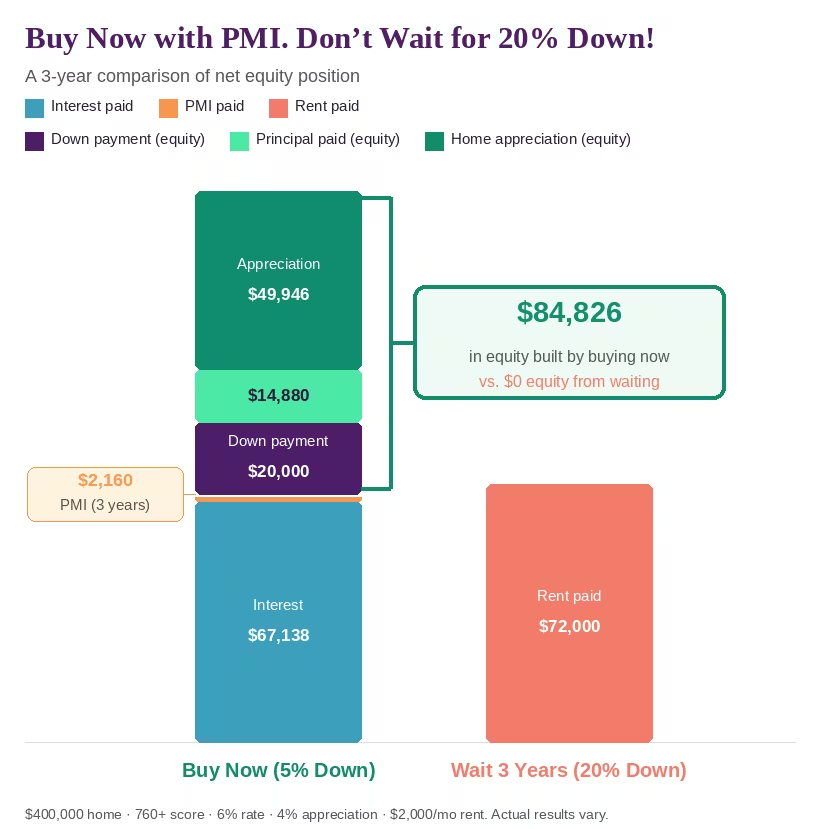

The math is clear: over 3 years, a buyer with 5% down and a 760+ score spends $69,298 in interest and PMI — but builds $84,826 in equity from their down payment, principal payments, and home appreciation. A renter waiting to save 20% burns $72,000 in rent with $0 in equity — and the home now costs $450,000 with a $90,000 down payment target instead of $80,000

We see buyers delay homeownership by 2–3 years to avoid a $06/month PMI payment, losing tens of thousands in equity and appreciation. PMI isn't a penalty — it's the cost of accessing homeownership with less cash. At rates.altgage.com, you can see your personalized payment estimate on any home in seconds.

FHA loans have MIP, not PMI

FHA uses flat mortgage insurance premium or MIP (0.55%), which is cheaper below 680 FICO. Above 680, conventional PMI wins. See our full FHA vs conventional comparison. Above 680, conventional PMI drops below FHA MIP — and the gap widens fast. At 740+, conventional PMI is half the cost of FHA. At 780+, it's roughly a third.

The monthly payment is only half the story. FHA MIP is permanent on FHA loans with less than 10% down The only way to eliminate it is to refinance into a conventional loan once you have enough equity — which means paying closing costs again. Conventional PMI, by contrast, cancels automatically at 78% LTV. FHA charges upfront MIP too. FHA adds a 1.75% upfront mortgage insurance premium ($6,755 on a $386,000 loan), typically rolled into the loan balance. This increases your total loan amount and the interest you pay over the life of the mortgage. Conventional loans have no equivalent upfront charge.

What if your loan exceeds the FHA limit? FHA loan limits vary by county — in 2026, the standard limit is $541,287 and the high-cost ceiling is $1,209,750. If the home you're buying pushes your loan above the FHA limit for your area, conventional is your only option. In that scenario, a credit score boost before closing isn't just helpful — it's the primary lever you have to control your PMI cost. A rapid rescore that moves you from 680 to 720 saves $127/month in PMI on a $380,000 loan.

The Bottom Line

PMI is avoidable, but the bigger question is whether avoiding it is actually worth the cost. For buyers with 740+ credit, PMI adds a modest $60–$92/month that cancels automatically — and it unlocks homeownership years earlier than saving for 20% down. If your PMI quote seems high, don't blame the down payment — check your credit score. A 60-point improvement saves more per month than an extra $40,000 in down payment. That's the real leverage point. Check your rate at Altgage to see your personalized PMI estimate and explore whether buying now with PMI beats waiting to save 20%.

Frequently Asked Questions

When does PMI go away?

On conventional loans, your lender must automatically cancel PMI when your loan balance reaches 78% of the original home value. You can also request cancellation at 80% LTV. With home appreciation, many buyers reach this threshold faster than their amortization schedule suggests.

Is it worth paying for PMI?

Absolutely, it's almost always better to buy now with PMI and a good credit score. If not you'll give up home price appreciation while paying rent and struggling to accumulate and ever increasing down payment.

Is PMI tax deductible?

The PMI tax deduction has been available in some years but not others — Congress has periodically renewed it. Check with a tax professional for the current status, as it may affect your effective PMI cost.

Can I avoid PMI with an FHA loan?

No — FHA loans have their own mortgage insurance (MIP) that works differently. FHA MIP is a flat 0.55% so it's more expensive than conventional PMI for borrowers with 700+ credit scores, and the annual MIP on FHA loans with less than 10% down lasts for the life of the loan (it never cancels). If your credit score is less than 680, an FHA loan with MIP costs less overall.