.avif)

.avif)

Buying a home is exciting - but let’s be honest, figuring out the money part? Not so much. Between saving for a down payment and navigating loan options, the process can quickly feel overwhelming.

One moment you're picturing your dream kitchen, and the next, you're googling terms like “jumbo loan” and “conventional loan” wondering what they even mean. Don’t worry - you’re not alone. Let’s clear the confusion and break down the real difference between these two popular loan types, so you can move forward with confidence.

What is a Jumbo Loan?

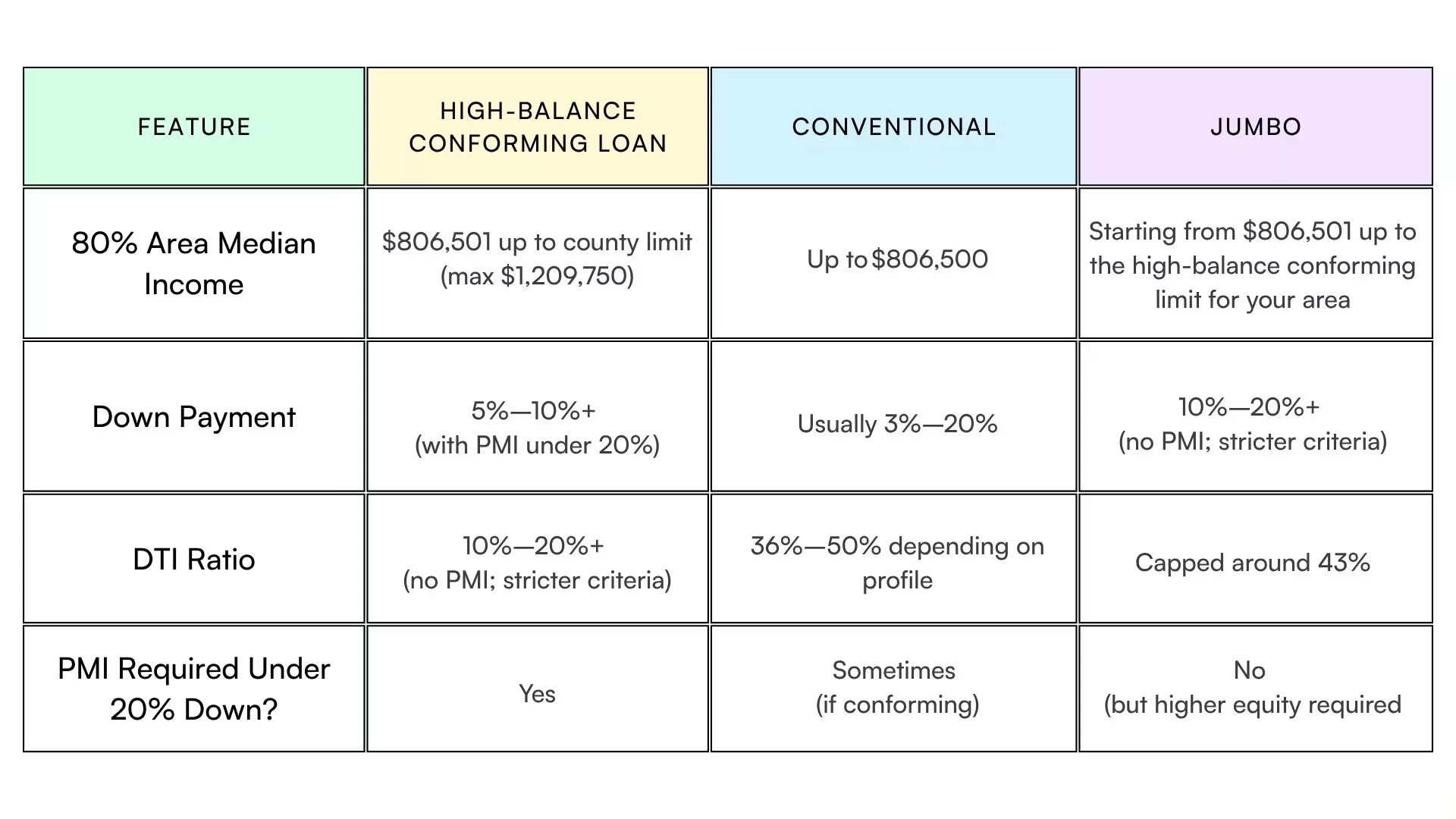

A jumbo loan is a type of mortgage used to finance homes that are too expensive for a conventional loan. If the amount you need to borrow exceeds the conforming loan limit in your area (for 2026, that’s $832,750 in most parts of the U.S.), you’ll need a jumbo loan.

Because these loans are not backed by Fannie Mae or Freddie Mac, they come with higher risks for lenders. That means stricter requirements for borrowers.

Jumbo Loan Requirements

Since jumbo loans involve larger amounts of money, the approval process is a bit more demanding:

- High credit score: Typically 680 or above.

- Large down payment: Minimum down payment of 20%, sometimes more.

- Low debt-to-income ratio: Debt-to-income ratio should be under 43%.

- Full documentation: You’ll need to provide proof of income, tax returns, and bank statements.

In short, jumbo loans are for financially strong buyers who are purchasing luxury or high-priced homes. Get approved in a day!

What is a Conventional Loan?

A conventional loan is the most common type of home loan in the U.S. It's not backed by the government like FHA, VA, or USDA loans. Instead, it's offered by private lenders such as banks, credit unions, and mortgage companies.

Conventional loans usually follow rules set by two big government-sponsored enterprises - Fannie Mae and Freddie Mac. These organizations don’t lend money themselves, but they buy loans from lenders. To be eligible for this backing, loans must meet certain size limits and guidelines.

The key thing to remember: if you’re buying a home within your area's conforming loan limit (set by the Federal Housing Finance Agency), then you’re likely dealing with a conventional loan.

Example: Let’s say you want to buy a home in an area where the conforming loan limit is $832,750 (the baseline limit for most areas in 2026). If you’re purchasing a home for $750,000, you can apply for a conventional loan with a 5% down payment of $37,500, meaning you'd need to borrow $712,500 - which keeps you within the conventional loan limit.

See today’s rate and get an estimate in 10 seconds…

Conventional High-Balance Loans

Not all loans above $832,750 are classified as Jumbo loans. In certain high-cost real estate markets - such as parts of California, New York, Hawaii, and areas like Miami, Florida - you may qualify for a high-balance conforming loan instead.

What Is a High-Balance Loan?

A high-balance loan is a conventional mortgage that exceeds the standard conforming loan limit of $832,750 (as defined by the Federal Housing Finance Agency – FHFA) but remains below $1.2 million, depending on your location. These loans are designed for buyers in expensive housing markets, allowing them to borrow more without moving into the Jumbo loan category.

Want to know your local high-balance limit?

Use this official FHFA lookup tool → Check Your County Limit (FHFA.gov)

Benefits of High-Balance Loans

- Lower down payment requirement: You can qualify without putting 20% down.

- Competitive interest rates: These loans typically offer lower rates than Jumbo loans, though slightly higher than standard conforming loans.

- Larger loan amounts: You get access to larger financing options while still benefiting from conventional loan perks, including easier approval standards and lower PMI.

- Ideal for expensive markets: Perfect for homebuyers in high-cost areas who want more purchasing power with less upfront cost.

Conventional Home Loan Requirements

To qualify for a conventional loan, you’ll need to meet a few basic requirements:

- Good credit score: The min score is 620, but practically 680+ is recommended for better rates, more affordable PMI and a higher chance of approval.

- Down payment: It’s a min of 3% for first-time buyers or 5% of the home’s purchase price for everyone else. A 20% down payment helps you avoid private mortgage insurance (PMI), but PMI is the best deal on homeownership money can buy.

- Stable income and employment history: Lenders like to see two years of consistent employment.

- Debt-to-income (DTI) ratio: Generally should be under 50% for housing and non-housing debts.

Conventional loans work best for buyer

Which Loan is Right for You?

Choosing between a jumbo loan and a conventional loan comes down to your budget, credit profile, and the price of the home you want to buy. Ask yourself a few questions:

- What’s the price of the home?

- How much can I afford to put down?

- Do I have strong credit and a stable income?

- Will I qualify for a loan under the conforming limit?

Your answers will help steer you in the right direction.

Smart and Affordable Mortgage Options with Altgage

When it comes to choosing the right loan, having the right partner can make all the difference. At Altgage, we offer smart and affordable mortgage solutions tailored to your unique financial needs. Whether you're looking for a standard conforming loan, a high-balance conforming loan for high-cost areas, or exploring jumbo loan options, we are here to simplify the process, offer competitive rates, and guide you every step of the way.

With Altgage, you’ll get personalized advice, powerful tools, and a stress-free home financing experience - so you can focus more on finding your dream home and less on navigating the mortgage maze.

Whether you go with a conventional loan or a jumbo loan depends on your financial situation and the home you’re aiming to buy.

Before you decide, talk to a trusted lender or mortgage advisor like Altgage. They can help you compare your options, run the numbers, and make sure you’re making the best move for your future home.