Most homebuyers think they have two choices: 15-year or 30-year mortgages. But there's a third option that's often overlooked—the 20-year mortgage. It delivers massive interest savings with lower rates and a lower term, while also keeping payment affordable. 15-year mortgages typically double the payment increase relative to 20-year mortgage but for only half the additional savings. Here are few reasons why 20-year mortgages are gaining popularity among savvy homebuyers:

Why 20-year mortgages rates are lower than 30-year rates

20-year mortgages typically offer rates 0.25% to 0.50% lower than 30-year mortgages because lenders view them as less risky. Shorter loan terms mean reduced exposure to interest rate changes and default risk. This allows lenders to offer better rates that fall between 15-year and 30-year options.. That rate difference alone saves you tens of thousands, even before considering the shorter term. A shorter loan further amplifies your total interest savings and reduces the overall cost of your loan. Mortgage rates are based on the 10-year Treasury plus a premium. The premium for 20-year mortgages is 0.25-0.5% lower than 30-year premiums. Some lenders use a weighted average of 7-year and 10-year Treasury rates for 20-year pricing, creating additional rate advantages.

1. Reduced Credit Risk

- Shorter duration = less default risk over the loan's lifetime

- Borrowers qualifying for 20-year terms typically have stronger financial profiles

2. Lower Interest Rate Risk for Lenders

- Duration risk: Lenders face less exposure to interest rate changes

- 20-year loans have lower "duration" (price sensitivity to rate changes)

3. Prepayment Risk Dynamics

- Faster principal paydown reduces lender's outstanding exposure

- Lower refinancing risk compared to 30-year loans

- More predictable cash flows for mortgage investors

Current typical rates:

- 30-year mortgage: 6.125%

- 20-year mortgage: 5.750%

To get an accurate rate quote, check 20-year mortgage rates pam.altgage.com/rates

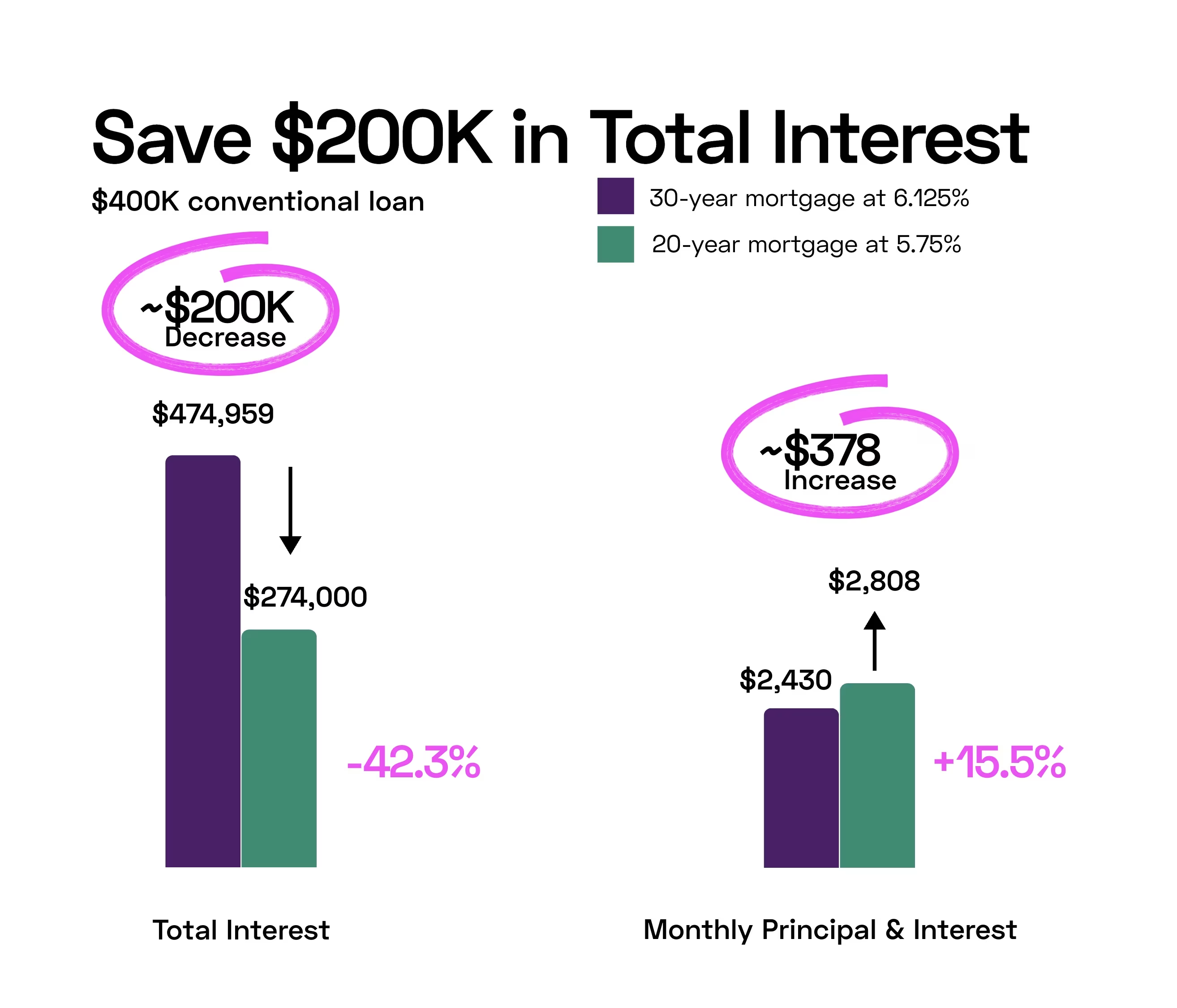

$200,000 of interest savings: 20-year vs 30-year comparison

Total mortgage interest depends on your loan amount, interest rate, and loan term. This can be expressed as TIP (total interest percentage)—the total interest paid relative to the loan amount. Because mortgages are amortized, TIP is fixed for every rate and term combination. At the same interest rate, TIP is proportional to the loan length; therefore, all other things being equal, a 20-year loan will save you about 50% of your loan amount in interest savings.

You save $200K+ in interest for just $378 more per month. That's $500+ of lifetime interest saved for every extra dollar you pay monthly. Payments remain affordable with a 15% increase in principal and interest—less than $100 per month for every $100,000 of loan amount. In this example, on a $ 400,000 loan, P&I will increase from $2,430 to $2,808. Including Taxes and Insurance, PITIA may jump from $3,100 > $3,500. If you earn $10,000 a month, the housing debt-to-income ratio remains conservative at 35%.

Be debt-free 10-years faster

A 20-year mortgage isn't a FIRE (Financial Independence, Retire Early) scheme, but who wants to pay a mortgage for 30+ years? Buy your first home at 35, and you'll approach retirement before it's paid off. Take your last mortgage at 50, and you might never see it fully paid. There’s a reason it’s called a mortgage; the root "mort" means death, and "gage" means pledge. 20-year mortgage helps eliminate this “dead-pledge” for debt-free living. Once your mortgage is paid off, the money that was previously allocated to your monthly payment is now free to be directed towards other financial goals. This significant increase in disposable income can accelerate your retirement savings or fund a child's approaching college expenses.

Add 100% more towards mortgage principal

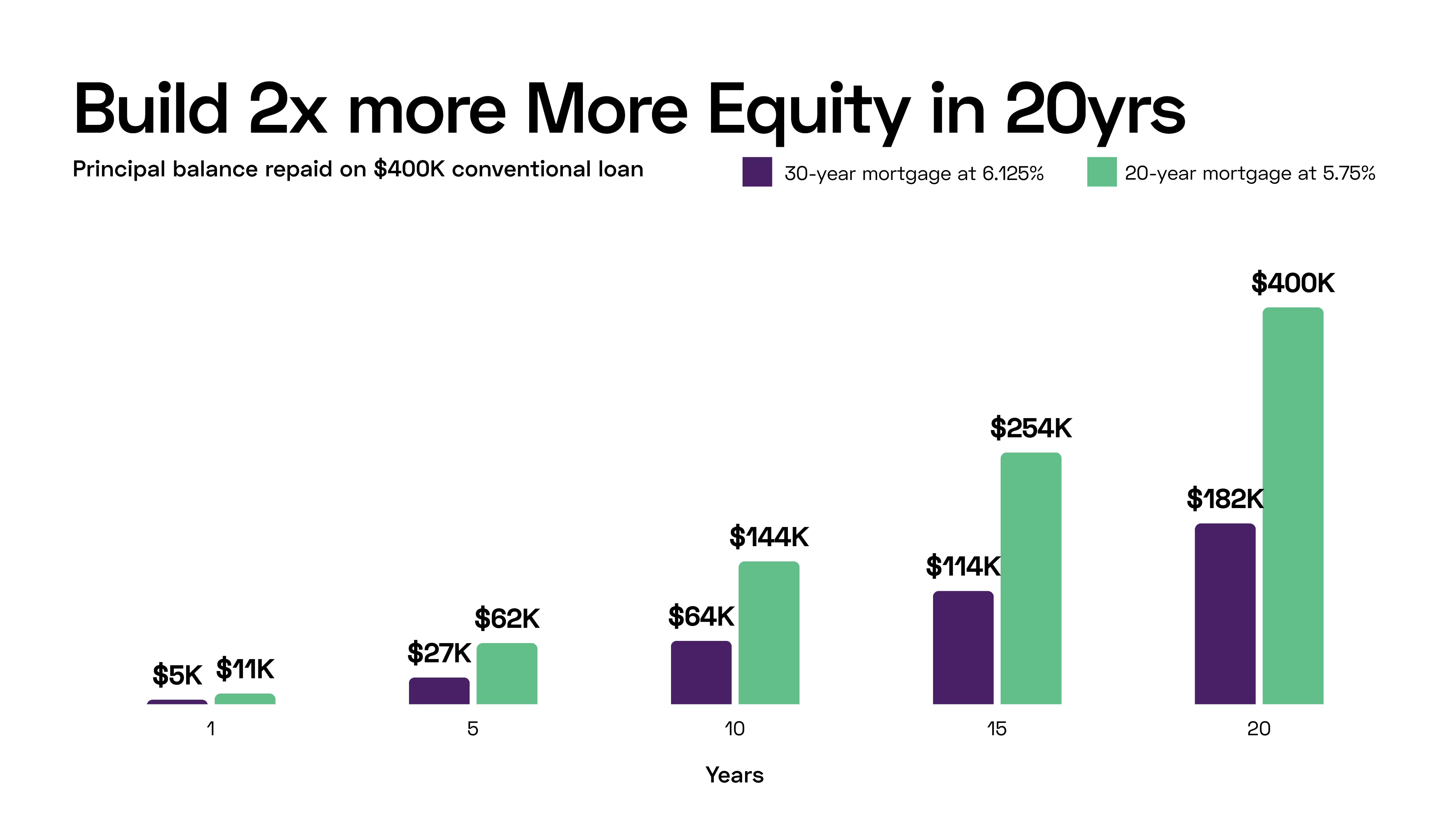

A key feature of 20-year mortgages is faster equity building. Mortgages pay interest first and in full. Shorter terms and lower rates mean a higher portion of your payment goes toward principal. In fact, more than 2x of your mortgage payment goes towards principal in a 20-year loan. Did you know that a majority of your mortgage principal on a 30-year mortgage is repaid during the last 10-year. Let’s take a look the amount of equity built in year 10 of a 30-year loan vs a 20-year loan

$144K vs 64K in year 10 is 125% higher or 2.25X more. These difference can be much more stark at the 15 or 20-year mark when the loan is paid in full. Imagine moving at year 5 and having to shell out 8% of your homes value in transaction costs. You’d lose out on all your hard earned equity. There is some nuance here because homes also appreciate each year, so buying a home for 5yrs on a 30-year note may still make sense. The above example is for illustration purposes. It is unlikely that a home does not appreciate.

Should I get a 20-year mortgage?

A 20-year mortgage makes sense if you:

✅ Can comfortably afford the higher monthly payment i.e., housing DTI is <35%

✅ Want to build equity faster and stay in your home for at least 7yrs

✅ Prefer guaranteed savings over investment risk

✅ Want to be mortgage-free before retirement

When you shouldn't choose a 20-year mortgage

1. Cash Flow Inflexibility - Higher monthly payments reduce financial flexibility for unexpected expenses

2. Opportunity Cost of Capital - Investment returns may exceed mortgage savings in strong market periods. You also have lower liquidity compared to investing the extra payment amount.

3. Employment/Income Risk - Higher payments make it harder to qualify for loan modifications during financial hardship. The risk of foreclosure also increases with higher payment obligations.

Here are a few scenarios in which you should not choose a 20-year mortgage

❌ Debt-to-income ratio above 35% (including the 20-year payment)

❌ Irregular income (commission, freelance, seasonal work)

❌ Minimal emergency savings (less than 6 months expenses)

❌ Plans to move within 5-7 years

❌ Significant other high-interest debt (credit cards, personal loans)

❌ Career transition periods (job changes, industry shifts)

❌ Single-income households without backup income sources

Don't default to a 30-year mortgage just because "everyone does it." For many homebuyers, especially those whose incomes are expected to increase over time, the 20-year mortgage is the sweet spot between affordability and savings.

Get started: Check 20-year mortgage rates

While 20-year mortgages offer significant advantages, they're not right for everyone. The higher monthly payments reduce financial flexibility and may limit your ability to handle unexpected expenses or take advantage of investment opportunities. Consider your job stability, emergency savings, and long-term plans before committing to the higher payment structure. 20-year mortgages work best for borrowers with stable incomes, adequate emergency funds, and plans to stay in their home for at least 7 years. If you have irregular income, minimal savings, or significant other debt, a 30-year mortgage may provide better financial security despite the higher total interest cost. Ready to see how much you could save? Check current 20-year mortgage rates or start your application to explore your options. The question isn't whether you can afford a 20-year mortgage—it's whether you can afford not to consider one.