You have equity in your home. You want to use some of it. The two most common ways to do that are a home equity line of credit (HELOC) and a cash-out refinance. Both let you borrow against your home's value—but the mechanics, costs, and consequences are completely different. If you're new to HELOCs, start with our complete HELOC guide.

Here's the short version: if you locked in a mortgage rate below 5% anytime before 2023, a cash-out refinance almost certainly costs you more in the long run. A HELOC lets you borrow on top of that low rate instead of replacing it.

But "almost certainly" isn't "always." This guide walks through the full comparison so you can make the right call for your situation.

There's also a third path worth knowing about: a home equity loan, which gives you a fixed-rate lump sum without a draw period. We cover that in our HELOC vs. home equity loan comparison.

How Each One Works

Cash-Out Refinance

A cash-out refinance replaces your entire existing mortgage with a new, larger loan. You receive the difference between the new loan amount and your old balance as cash.

Example: You owe $300,000 on your current mortgage. Your home is worth $450,000. You refinance into a new $360,000 mortgage and receive $60,000 in cash (minus closing costs). Your old mortgage is gone—your new mortgage is the only one.

The new mortgage carries today's interest rate, applied to the entire $360,000 balance—not just the $60,000 you're pulling out.

HELOC

A HELOC is a second lien on your property. Your existing mortgage stays exactly as it is—same rate, same balance, same payment. The HELOC sits on it, giving you access to a credit line secured by your equity.

Example: Same $300,000 mortgage on a $450,000 home. You open a $60,000 HELOC. You now have two obligations: your original mortgage (untouched) and the HELOC. You only pay interest on the HELOC amount you actually draw.

Altgage's Primary HELOC Partner: Figure

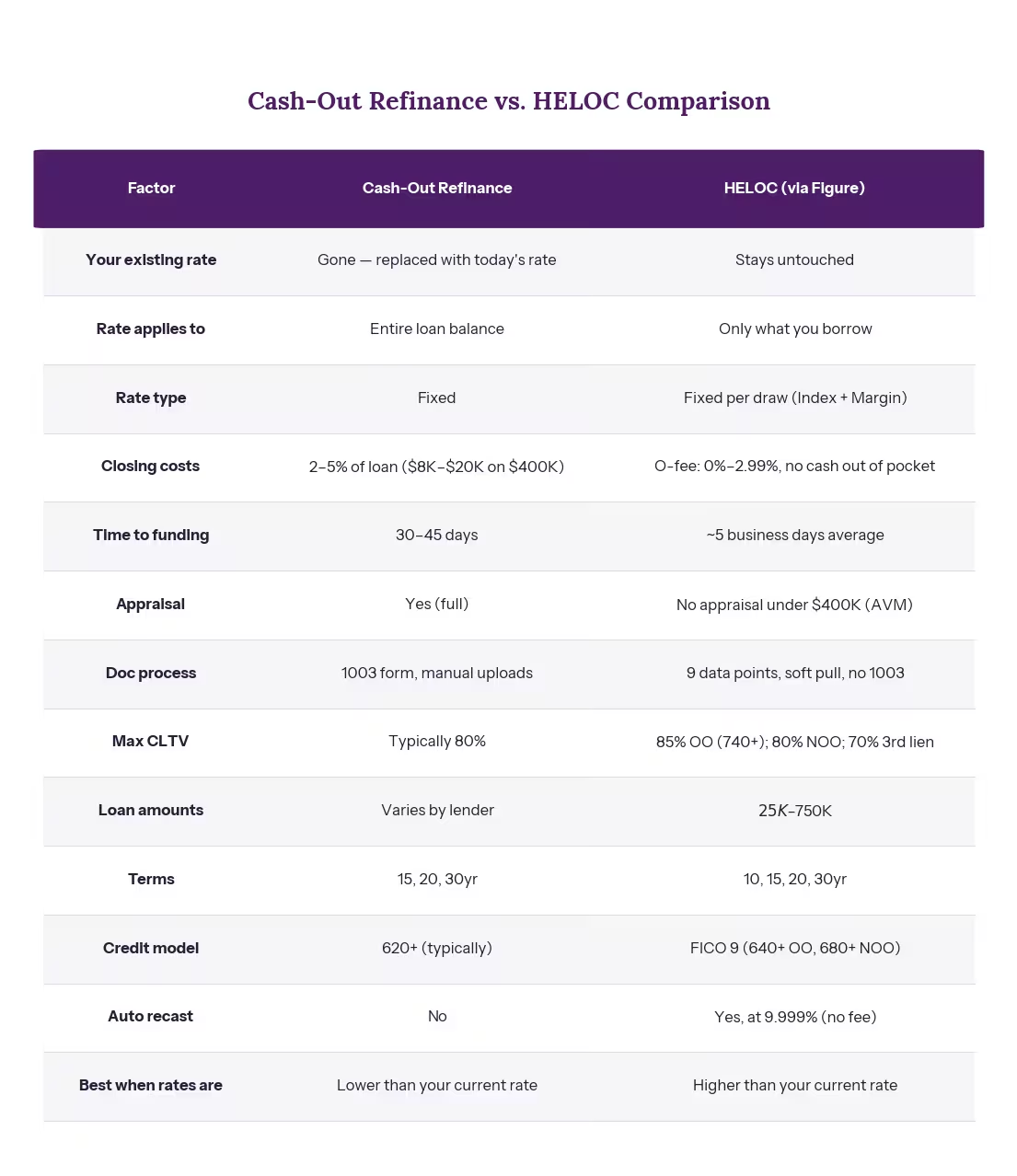

Altgage partners with Figure—a blockchain-powered lender—as our flagship HELOC provider. Figure's automated underwriting system delivers rates in minutes and funds in as little as 5 business days, using just 9 data points (soft credit pull + AVM, no appraisal for loans under $400K). You pay interest on a fixed rate that's locked per draw, fully amortizing, with no prepayment penalties.

The Comparison That Matters

The Rate Math: Why This Decision Is Mostly About Your Current Mortgage

This is where most guides get vague. Let's use real numbers.

Scenario: You have a $350,000 mortgage at 3.25% (locked in 2021). You want to access $50,000 in equity. Current market rates: ~6.75% for a cash-out refi.

Option A: Cash-Out Refinance

New mortgage: $400,000 at 6.75%. Your monthly payment jumps from ~$1,523 to ~$2,594. That's an increase of $1,071 per month—but only $50,000 of that new balance is "new money." You're paying the higher rate on your original $350,000 too.

Over the life of the loan, the rate increase on the existing balance alone costs you roughly $140,000 in additional interest. For $50,000 in cash.

Closing costs (2–5% of $400K) add $8,000–$20,000 upfront or rolled into the loan, which increases the amount you're financing and the total interest paid.

Option B: HELOC via Figure

Your original mortgage stays at $1,523/month. You open a Figure HELOC for $50,000 with a fixed rate per draw. The HELOC rate depends on your CLTV, FICO, and origination fee tier.

Origination Fee Tradeoffs (no cash out of pocket):

- 0% fee: higher rate

- 0.99% fee: moderate rate

- 1.99% fee: lower rate

- 2.99% fee: lowest rate

The lowest-cost scenario: 2.99% origination fee rolled into the $50,000 (adds ~$1,495 to your balance). On a 30-year amortization, that adds roughly $10/month.

Let's say your Figure HELOC rate is 7.5% with a 1.99% fee ($995 rolled in). The payment on $50,000 is roughly $350/month (30yr, fully amortizing). Total: $1,873/month.

Monthly savings vs. cash-out refi: $721/month, and you keep your 3.25% rate on the $350K.

Why the fee structure matters: Figure's origination fees range from 0% to 2.99%. A lower fee means you borrow less (the fee itself isn't paid out of pocket—it's added to your loan balance). Higher fees come with lower rates. You choose which tradeoff makes sense for your timeline and rate environment.

Altgage Perspective

The rule of thumb is simple: if today's rates are higher than your existing mortgage rate, a HELOC protects your low rate. If today's rates are lower, a cash-out refinance lets you improve your rate on the full balance while accessing equity.

For HELOC borrowers, Figure's 5-day funding and zero-appraisal process (under $400K) eliminate much of the speed advantage that refinances once held. You also get fixed rates per draw with no prepayment penalties and options to recast automatically when rates hit 9.999%.

Altgage shops multiple HELOC and home equity lenders — each with different CLTV limits, credit requirements, and fee structures — to find the best fit for your situation. For Figure-specific rates and terms, start at rates.altgage.com.

When a Cash-Out Refinance Still Wins

Your current rate is at or above today's rates. If you're sitting on a 7.5% mortgage from late 2023, refinancing into 6.75% lowers your rate on the full balance AND gives you cash. Clear win.

You need a large amount of cash ($100,000+). HELOCs max out based on available equity and CLTV limits. Figure caps individual loans at $750K and CLTV at 85% (80% for non-owner-occupied), so very large cash pulls may hit those boundaries. A cash-out refi on a high-value property may give you more room.

You want to consolidate a first and second mortgage. If you already have a HELOC or second lien with a high rate, rolling everything into one new first mortgage simplifies your payments and may lower your blended rate.

You plan to stay in the home for 15+ years. The fixed rate and single-payment structure of a refi can be advantageous over very long horizons, even at a slightly higher rate.

When a HELOC Is the Better Move

You have a low first mortgage rate (sub-5%). This is the majority of homeowners who bought or refinanced between 2019 and early 2022. Protecting that rate is worth a higher per-dollar cost on the HELOC.

You need a smaller amount ($25,000–$100,000). Figure's minimum loan size is $25K. The proportional savings of keeping your low first mortgage rate get more dramatic as the HELOC amount shrinks relative to your total balance.

You want speed. Figure funds in as little as 5 business days using blockchain-powered automated underwriting. No appraisal under $400K, no 1003 form, no manual doc uploads. That's roughly 6–8 times faster than a cash-out refi at 30–45 days.

You want flexibility. Many HELOCs offer a draw period where you can access funds as needed, pay them down, and redraw. A cash-out refi is a one-time event. Figure's 100% initial draw at closing means you get your full approved amount upfront, then draw and repay as needed.

You're using it for a time-limited purpose. Bridge financing, debt consolidation you'll pay off quickly, or a home renovation with a known budget—a HELOC lets you pay it down without refinancing again. Figure's no prepayment penalties mean you can accelerate repayment without penalty if your circumstances change.

You want fully amortizing payments with no balloon. Figure's fixed-rate HELOC is fully amortizing, so your rate and payment structure are completely transparent from day one. No ARM surprises, no draw-to-repayment conversion shock.

What About Closing Costs?

Cash-out refinances carry closing costs of 2–5% of the total loan amount. On a $400,000 refi, that's $8,000–$20,000. These can be rolled into the loan, but that means you're borrowing more—and paying interest on the closing costs themselves.

Figure HELOC closing costs are structured as origination fee options:

- 0% origination fee: Highest rate; zero upfront cost

- 0.99% origination fee: Moderate rate; $500 fee on a $50K loan, rolled into balance

- 1.99% origination fee: Lower rate; $995 fee on a $50K loan, rolled into balance

- 2.99% origination fee: Lowest rate; $1,495 fee on a $50K loan, rolled into balance

No other closing costs. No appraisal fees (under $400K). No title insurance required. No 1003 form fees. No manual document upload processing. This is a fundamental difference from cash-out refi closing costs, which typically include appraisal ($400–$600), title insurance, origination, processing, underwriting, wire transfer, and other fees—totaling 2–5%.

The cost difference is substantial. A $50K Figure HELOC with a 2.99% fee costs ~$1,495 rolled into the loan. A $400K cash-out refinance with 3% closing costs costs ~$12,000.

Tax Implications

Interest on both products may be tax-deductible if the funds are used to "buy, build, or substantially improve" your home. This applies to up to $750,000 in combined mortgage debt under the Tax Cuts and Jobs Act.

If you use either product for debt consolidation, a vacation, or other non-home-improvement purposes, the interest is not deductible. The tax treatment is the same regardless of which product you choose—what matters is how you use the funds, not the loan type.

Figure HELOC: Additional Details

Credit Requirements: 740+ FICO for 85% CLTV (owner-occupied). 680+ for 70% CLTV (3rd lien, owner-occupied). FICO 9 credit model used.

Loan Range: $25,000–$750,000.

Terms: 10, 15, 20, or 30 years.

Rate Structure: Fixed rate per draw (Index + Margin). Margin varies based on CLTV, FICO, and origination fee tier. For exact rates, see rates.altgage.com.

Auto Recast: Automatic recast available at 9.999% (no fee).

Underwriting Process: 9 data points → soft credit pull + automated valuation (no appraisal under $400K) → rate/pricing in minutes → automated income verification → 5-day funding.

Not Recommended For:

- Self-employed borrowers (simplified documentation not available)

- NY residents (not available in NY)

Availability: CA, MA, TX, FL, CO, GA

Frequently Asked Questions

Is a HELOC or cash-out refinance better right now?

For most homeowners in 2026, a HELOC is the better choice. The majority of existing mortgage holders locked in rates between 2.5% and 5% during 2019–2022. Replacing those rates with today's rates (mid-6% to 7%) through a cash-out refi costs significantly more over the life of the loan than a HELOC on the smaller borrowed amount.

Figure's speed (5-day funding), zero appraisal under $400K, and fee flexibility make HELOCs competitive or superior to refinancing on almost every metric except rate improvement on your first mortgage.

Can I get a cash-out refinance if I already have a HELOC?

Yes. A cash-out refinance pays off both your first mortgage and any existing HELOC, replacing them with a single new loan. If your HELOC rate has climbed and you no longer need the flexibility, consolidating into a fixed-rate first mortgage can simplify your finances.

Does a HELOC affect my ability to refinance later?

It can. If you have an outstanding HELOC balance, a future refinance lender will need the HELOC lender to agree to subordination (accepting second-lien position behind the new first mortgage). Figure typically grants subordination, but it adds a step and can cause delays.

What credit score do I need for a HELOC vs. a cash-out refinance?

Figure HELOC: 640+ for owner-occupied primary residences (1st or 2nd lien); 680+ for investment properties, second homes, and 3rd liens; 760+ for loan amounts above $400K. A 740+ score unlocks the best CLTV (up to 85%) and rate terms.

Cash-Out Refinance: Typically 620+. You'll get better rates at 700+ on either product.

If your score needs improvement, a rapid rescore strategy may help.

Can I do both?

Yes. Some homeowners maintain their low-rate first mortgage, take a Figure HELOC for immediate needs, and plan to refinance everything later if rates drop significantly. This "wait and layer" strategy preserves optionality. Figure's no prepayment penalty means you can accelerate payoff of the HELOC without penalty if refinancing becomes attractive.

What about a home equity loan instead?

A home equity loan is a third option that gives you a lump sum at a fixed rate with no draw period. It protects your first mortgage rate just like a HELOC but offers completely predictable payments. Note that some home equity loan lenders restrict the product to primary residences and second homes — investment properties may not be eligible. Read our HELOC vs. home equity loan comparison for the full analysis.

What if Figure isn't available in my state or my income situation?

Figure is currently available in CA, MA, TX, FL, CO, and GA. If you're outside those states or self-employed (where Figure's process isn't recommended), Altgage shops other HELOC lenders like SpringEQwith different geographic reach and income documentation flexibility. Start at rates.altgage.com to explore all available options.

The Bottom Line

The cash-out refinance vs. HELOC decision comes down to one question: is your current mortgage rate worth protecting? If yes—and for most homeowners right now, it is—a HELOC lets you access equity without sacrificing the rate you locked in when rates were historically low.

If your current rate is already at or above today's market, a cash-out refi lets you improve your rate and pull cash in one move.

Figure's 5-day funding, zero-appraisal process (under $400K), blockchain-powered underwriting, and flexible origination fee structure make HELOCs a faster and often cheaper path to cash than they were even three years ago. But the fundamental decision logic remains the same: compare your existing mortgage rate to today's rates, then choose the product that best preserves your advantage or takes advantage of improved rates.

Either way, compare both options with actual numbers before committing. No single lender is best for every borrower — CLTV limits, credit requirements, state availability, and income documentation all vary. As a mortgage broker, Altgage shops multiple lenders including Figure to find the best combination of rate, terms, and timeline for your specific profile. Start at rates.altgage.com.

Related Reading on Altgage