You've been paying your mortgage for years. Your home has appreciated. Somewhere between the monthly payments and the rising Zillow estimate, you've built up something valuable: home equity.

A home equity line of credit (HELOC) lets you turn that equity into usable cash — without selling your home and without refinancing your existing mortgage. You can use it to renovate, consolidate debt, cover an emergency, or do what an increasing number of homeowners are doing: buy your next property.

This guide covers everything — how HELOCs work, how much you can borrow, what it costs, how to qualify, and how a HELOC compares to other ways of accessing your equity.

What Is a HELOC?

A home equity line of credit is a loan secured by your home that gives you access to a revolving credit line based on your equity. Equity is the difference between what your home is worth and what you still owe on your mortgage. If your home is worth $400,000 and you owe $250,000, you have $150,000 in equity. A HELOC lets you borrow against a portion of that — typically up to 80–90% of your home's value minus your mortgage balance, depending on the lender, your credit score, and your state. Try our HELOC calculator.

The key advantage of a HELOC over a cash-out refinance is that your existing mortgage stays untouched. You keep your current rate, current payment, and current lender. The HELOC sits as a separate lien — usually in second position behind your first mortgage. This matters enormously right now. Most homeowners who bought or refinanced between 2019 and early 2022 locked in rates between 2.5% and 5%. Replacing that rate with today's 6.5–7% through a cash-out refi would cost thousands per year in extra interest on the original balance. A HELOC avoids that entirely.

How Does a HELOC Work?

A HELOC has two phases:

The Draw Period (Typically 2–5 Years)

During the draw period, you can access funds up to your credit limit. As you repay, the available credit replenishes — similar to a credit card.

Important nuances that vary by lender:

- Initial draw requirements. Some lenders require you to draw a large portion — even 100% — of the line amount at closing. Others require 75% upfront. This means a HELOC may not work like a traditional "draw $500 at a time" credit line. Understand your lender's initial draw requirement before applying.

- Additional draws. After the initial draw, most lenders allow additional draws during the draw period. Figure, Altgage's primary HELOC partner, sets a $4,000 minimum per additional draw — with unlimited draws during the draw period and each draw locking in a fixed rate for the remaining term. As you pay down the principal, you can redraw up to your credit limit.

- Payment structure. Modern HELOC products are typically fully amortizing from day one — you pay both principal and interest every month, building equity immediately. This is different from older bank HELOCs that offered interest-only payments during the draw period, which led to payment shock when the repayment period started.

The Repayment Period (Typically 12–27 Years)

Once the draw period ends, you can no longer borrow against the line. You continue making monthly payments to pay off the remaining balance. With a fully amortizing HELOC, your payment stays the same or decreases after the draw period closes — no surprises.

Fixed Rate vs. Variable Rate

Traditional HELOCs have variable rates tied to the prime rate. When the Fed raises rates, your HELOC rate goes up. When they cut, it goes down.

Many lenders now offer fixed-rate HELOCs where each draw locks in a fixed rate at the time of withdrawal. This gives you the flexibility of a credit line with the predictability of a fixed loan. Figure offers fixed-rate HELOCs where the rate is locked at each draw — meaning you can take multiple draws at different rates if market conditions change during your draw period, and all rates remain fixed for the life of your loan.

Available Terms

HELOC terms vary by lender. Figure offers four standard terms designed for flexibility:

- 10-year: 3-year draw period + 7-year repayment

- 15-year: 4-year draw period + 11-year repayment

- 20-year: 4-year draw period + 16-year repayment

- 30-year: 5-year draw period + 25-year repayment

All terms are fully amortized — no interest-only options, no payment surprises.

How Much Can You Borrow?

Your borrowing limit depends on four factors:

1. Your Home's Value

Lenders use either a full appraisal or an automated valuation model (AVM) to determine your home's current market value. AVMs are faster and cheaper — Figure uses AVM valuation for loans under $400,000, eliminating the appraisal step and accelerating your timeline. Altgage works with lenders that offer both options.

2. Your Mortgage Balance

Your existing mortgage is subtracted from the maximum allowable loan amount. The less you owe, the more you can access.

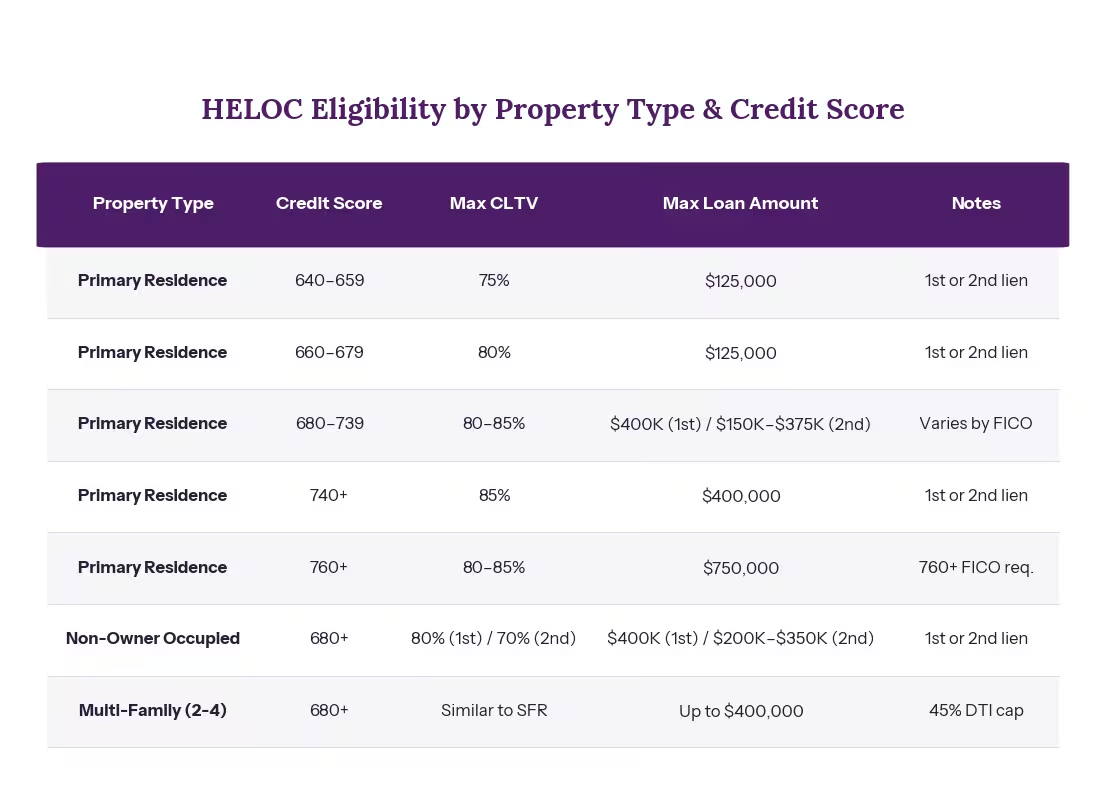

3. Maximum CLTV by Property Type and State

Combined loan-to-value (CLTV) is the total of all liens on your property divided by the home's value. Maximum CLTVs depend on your lender, credit score, property type, and state. Figure's CLTV structure is detailed below:

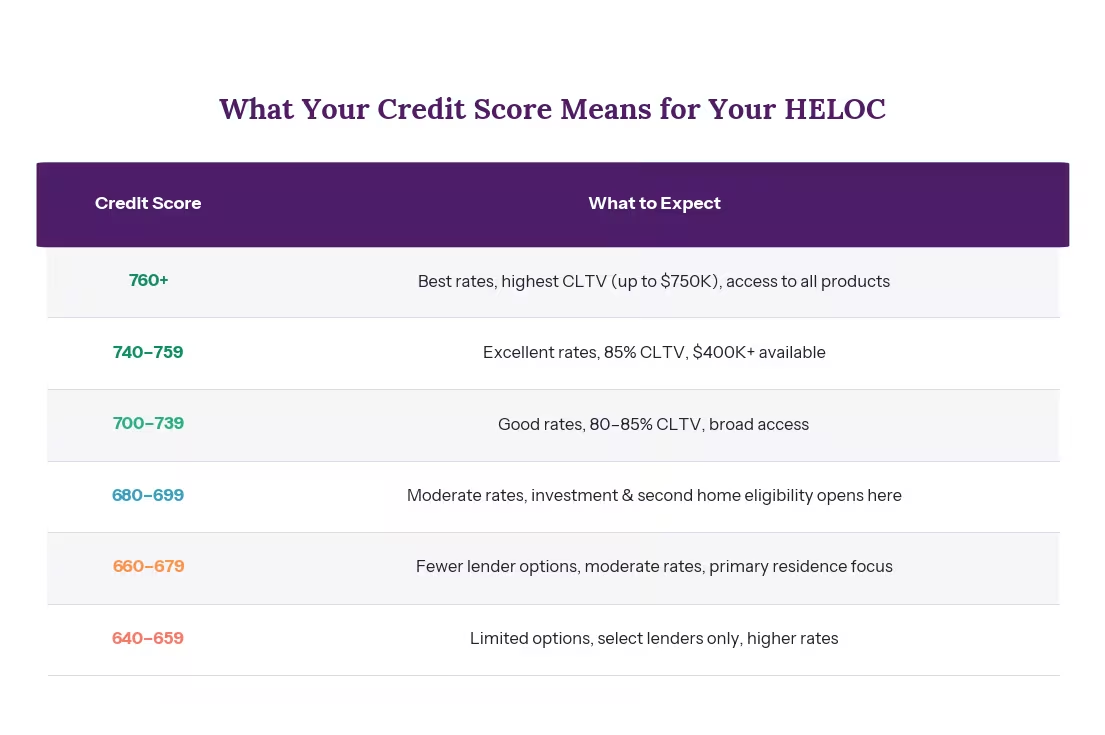

Example: Your home is worth $400,000 in California. You owe $250,000. With a 740 FICO, Figure allows 85% CLTV: $400K × 85% = $340K − $250K = $90,000 maximum HELOC. In Texas, the constitutional 80% cap applies, resulting in $320K − $250K = $70,000.

For investment properties (non-owner occupied), different FICO and CLTV tiers apply. Third-lien positions are available on owner-occupied properties only: up to $100,000 at 70% CLTV for borrowers with 680–759 FICO, and up to $150,000 at 70% CLTV for 760+ FICO.

4. Your Credit Score

Higher scores unlock higher CLTVs and lower rates. Minimums range from 640 to 680 depending on the lender and property type. Figure uses FICO 9, which weights medical collections and rental history more favorably than older credit models — a meaningful advantage if you have paid collections or consistent rent payment history.

If your score is in the 660–720 range, a rapid rescore strategy before applying could meaningfully improve your rate and available lender options.

Line Amounts

Figure offers lines from $25,000 to $750,000, with special underwriting for amounts over $400,000. Most lenders require minimums of $25,000–$60,000 depending on the state. Texas has a higher $35,000 minimum to account for state regulations.

What Can You Use a HELOC For?

There are no restrictions on how you use HELOC funds. The most common uses:

Home improvements. Kitchen, roof, addition, solar panels. Interest may be tax-deductible if the funds are used to substantially improve the home securing the HELOC.

Debt consolidation. Move 20%+ credit card balances to a 7–9% HELOC. On $50,000 in credit card debt, that's roughly $500/month in interest savings.

Buy your next property. Use the HELOC as a down payment on a second home, vacation home, or investment property. Your existing mortgage stays untouched. We cover the strategy, math, and risks in detail in our HELOC for investment property guide.

Bridge financing. Buy your next home before selling the current one, without making a contingent offer. Once your current home sells, you pay off the HELOC with the proceeds. Figure offers a dedicated bridge loan product with up to $400,000, available with origination fees of 2.99% or higher.

Emergency liquidity. An unused HELOC costs you nothing. Having a $50,000–$100,000 credit line available gives you a financial safety net without tying up cash.

Using a HELOC to Buy Property

One of the most powerful HELOC strategies is using your primary home's equity to fund the purchase of another property. There are three common scenarios:

Bridge Financing (Buy Before You Sell)

You've found your next home but haven't sold your current one. Instead of making a contingent offer, you open a HELOC on your current home and use it for the down payment. Once your current home sells, you pay off the HELOC with the proceeds. Total cost: a few months of HELOC interest — far less than the risk of losing the home you want.

Investment Property Down Payment

Open a HELOC on your primary residence, use the funds as a 20–25% down payment on a rental, and finance the rental with its own DSCR loan. The rental's cash flow covers its own mortgage and contributes toward paying down the HELOC. Repeat as you pay down and redraw.

Quick math: $60,000 HELOC draw at 8% = ~$440/month. If the rental generates $2,200/month against a $1,580 DSCR loan payment, you're cash-flow positive at $180/month even after the HELOC payment. As you pay down the HELOC, you restore borrowing capacity for the next deal.

One critical note: some home equity loan lenders (not HELOCs) restrict their product to primary residences and second homes only — investment properties are not eligible. Figure explicitly serves investment properties (non-owner occupied), making it ideal for this strategy.

For the full DSCR math, risk analysis, Texas homestead rules, and step-by-step strategy, read our dedicated guide: HELOC for Investment Property: Rules, Rates, and Strategy.

Second Home or Vacation Property

A HELOC can fund the down payment on a second home. CLTV limits are typically 70–80% (tighter than primary residences), and credit score requirements are usually 680+.

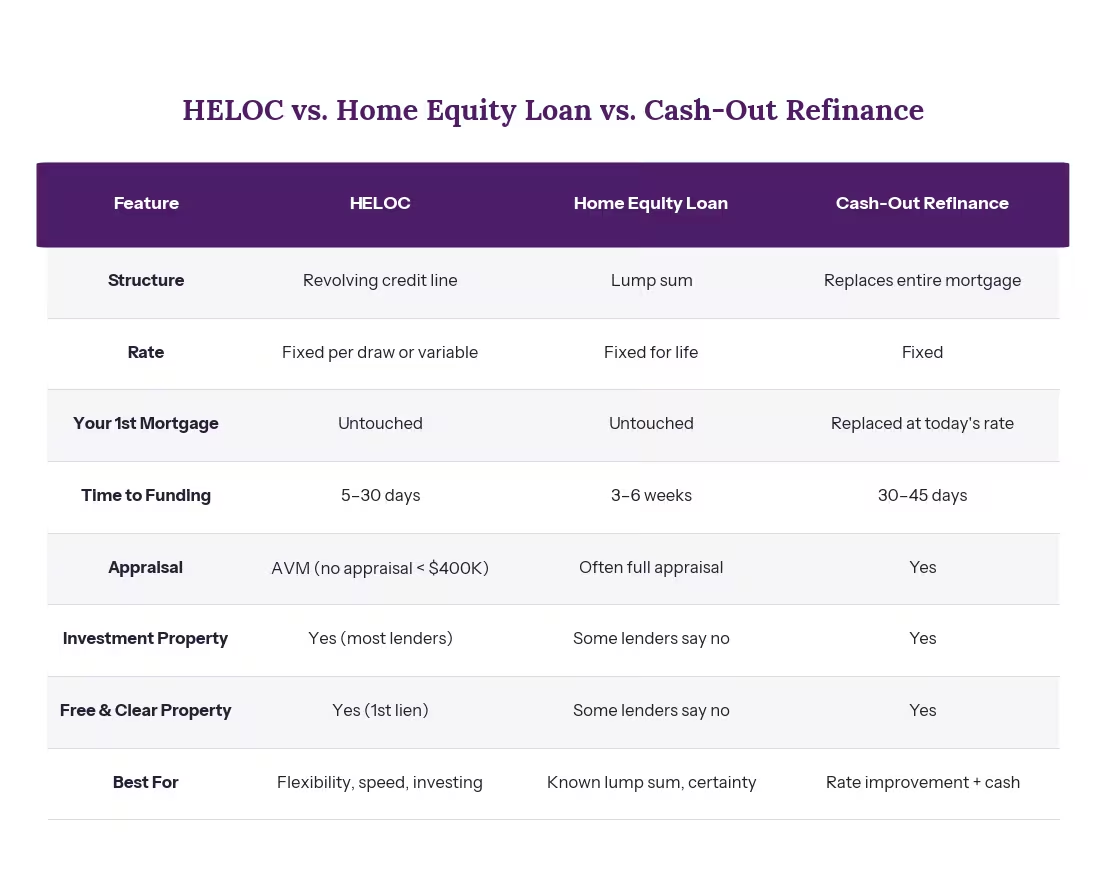

HELOC vs. Other Ways to Access Equity

A HELOC isn't your only option. Here's how the main products compare:

For detailed comparisons, read:

The HELOC Application Process

Step 1: Know Your Numbers

You need three data points: your home's approximate value, your current mortgage balance, and your credit score. Use the HELOC calculator to estimate your available equity and potential payment.

Step 2: Apply Through a Broker

HELOC lenders differ dramatically on CLTV limits, credit score minimums, rate structures, appraisal requirements, income verification methods, and which property types they serve. No single lender is best for every borrower. Altgage's primary HELOC partner is Figure — a blockchain-powered lender with some of the industry's fastest timelines, highest CLTV limits (up to $750,000), and lowest minimums for loan origination.

But Altgage also shops other lenders to ensure you get the best fit. A borrower with a 740 FICO might get 85% CLTV from Figure and a different maximum from another lender — that difference could mean $25,000+ in additional borrowing power on a $500K home.

Some lenders, including Figure, verify income automatically through payroll services, IRS.gov tax transcript linking, or bank statement analysis — no uploading W-2s or pay stubs. Others use traditional documentation and manual underwriting, which takes longer but can be more flexible for complex situations. Altgage matches you with the right process.

Step 3: Get Approved

The lender will do a soft credit pull (no impact to your score) and a home valuation — either an automated valuation (AVM) or a full appraisal. Figure uses blockchain-powered automated underwriting and AVM-based valuations for loans under $400,000, dramatically speeding the approval process. If everything checks out, you'll see your approved line amount, rate, and terms.

With Figure, you can typically see pricing and get approved in minutes.

Step 4: Review and Close

Review the terms carefully — especially the initial draw requirement, origination fee, draw period length, and whether the rate is fixed or variable. With Figure, the initial draw is 100% at origination (required for blockchain settlement), and all origination fees are rolled into the loan — no cash out of pocket. Closing is typically digital.

In Texas, there's a mandatory 12-day waiting period between your application and closing — the loan cannot close until 12 calendar days after you receive the required disclosure. After closing, you have an additional 3-business-day right of rescission before funds are disbursed. Plan for 3+ weeks total in Texas.

Step 5: Use Your Funds

After closing (and the rescission period, if applicable), funds are deposited directly. Use them for renovations, debt payoff, a property purchase, or whatever you need. Figure funds in approximately 5 business days on average.

Step 6: Repay Strategically

You only pay interest on what you draw. Many HELOC products, including Figure's, offer automatic recasting — if you make a lump payment exceeding 9.999% of the balance, your monthly payment automatically adjusts downward at no fee. This rewards aggressive repayment.

With Figure, there are no prepayment penalties — pay it off early at no cost.

HELOC Pros and Cons

Pros

- Protects your existing low mortgage rate. No refinancing required.

- Flexible access to funds. Draw what you need, pay it down, and redraw during the draw period.

- Faster than a refi or home equity loan. Some lenders, like Figure, fund in as few as 5 business days with minimal documentation.

- Lower upfront costs. Many products, including Figure, charge no out-of-pocket closing costs — all fees are rolled into the loan.

- Investment property eligible. Most HELOC lenders serve investment properties; many home equity loan lenders don't.

- Fixed-rate options now available. Eliminates variable-rate risk. Figure offers fixed-rate HELOCs with rates locked at each draw.

- No prepayment penalty. Pay it off early at no cost.

- Improved credit scoring models. Newer lenders like Figure use FICO 9, which treats medical collections and rental history more favorably.

Cons

- Your home is collateral. If you can't make payments, foreclosure is possible.

- Initial draw requirements. Some lenders require 75–100% of the line at closing. Figure requires 100% at origination, which ensures blockchain settlement but means you draw the full amount upfront.

- Origination fees. Some lenders charge up to 4.99%, rolled into the loan. Figure offers fee tiers from 0% to 2.99%.

- CLTV limits. In Texas, the constitutional 80% cap limits borrowing regardless of credit. Non-owner-occupied properties have stricter limits than owner-occupied.

- Not ideal for self-employed borrowers. Some programs work best for W-2 employees with documented income. Figure's automated income verification via IRS.gov and bank statements can help some self-employed borrowers, but complex business structures may be better served through Altgage's other equity products — non-QM loans, for example — that accept alternative documentation.

- Variable rate risk (on variable-rate products). If the prime rate rises, so does your payment. Choose a fixed-rate HELOC to eliminate this. Figure offers fixed rates only.

- State eligibility. Figure is not available in New York. Other states have specific restrictions (Texas has rate adjustments, Texas and New Mexico have CLTV caps, Florida condos have lower limits).

Frequently Asked Questions

What is a HELOC and how does it work?

A HELOC is a revolving credit line secured by your home's equity. You draw funds during a draw period (typically 3–5 years depending on your term), repay them, and can redraw. After the draw period, you repay the remaining balance over the remaining loan term (typically 7–25 years depending on your initial term). Modern HELOCs are fully amortizing — you pay principal and interest from day one, with no payment shock when the draw period ends.

Is a HELOC a good idea right now?

For most homeowners in 2026, yes — especially if you locked in a mortgage rate below 5%. A HELOC lets you access equity without replacing that low rate. With HELOC rates in the 7–9% range for qualified borrowers, it's significantly cheaper than credit cards (20%+) or personal loans (12%+), and faster than a cash-out refinance. If you need to bridge between properties, fund an investment, or consolidate debt, a HELOC is a powerful tool.

How much equity do I need for a HELOC?

You need enough equity to borrow at least the lender's minimum ($25,000 in most states, $35,000 in Texas) while staying within CLTV limits. Practically, you'll need at least 15–20% equity after accounting for your mortgage balance and the CLTV cap. Use the HELOC calculator to see your numbers.

What credit score do I need?

Minimums range from 640 to 680 depending on the lender and property type. Primary residences have the lowest requirements (Figure's minimum is 640). Investment properties and second homes typically require 680+. Higher scores unlock better rates — the difference between a 640 and a 760 can be a full percentage point or more. Figure uses FICO 9, which is more favorable to borrowers with medical collections or strong rental history.

Can I use a HELOC to buy another house?

Yes. You can use HELOC funds for any purpose, including a down payment on a second home, vacation property, or rental. The HELOC stays secured by your current home; the new property gets its own mortgage. Read our investment property guide for the full strategy and math.

How is a HELOC different from a home equity loan?

A HELOC gives you a revolving credit line with a draw period. A home equity loan gives you a one-time lump sum with fixed payments. Both protect your first mortgage. The biggest practical difference: most HELOC lenders serve investment properties, while some home equity loan lenders restrict to primary residences only. Read our full HELOC vs. home equity loan comparison.

Are HELOC rates fixed or variable?

Both options exist. Traditional bank HELOCs are variable (tied to the prime rate). Many newer products offer fixed rates — either for the full loan or locked at each draw. Figure offers fixed-rate HELOCs only, with rates locked at each draw. Altgage offers both fixed and variable-rate options depending on the lender.

Is HELOC interest tax deductible?

Yes, if funds are used to buy, build, or substantially improve the home securing the HELOC (up to $750,000 in combined mortgage debt). Interest on funds used for other purposes is generally not deductible as mortgage interest — though investment-related interest may be deductible on Schedule E. Consult a tax advisor.

How long does it take to get a HELOC?

It varies from 5 business days to 4 weeks depending on the lender and your situation. With Figure, you can often get approved in minutes and funded in approximately 5 business days. Automated processes (AVM + digital income verification) are fastest. Manual underwriting with a full appraisal takes longest. In Texas, add the mandatory 12-day pre-closing waiting period and 3-day post-closing rescission to any timeline — plan for 3+ weeks total.

Why should I get a HELOC through a broker?

CLTV limits range from 80% to 90%. Credit minimums range from 640 to 680. Some lenders use automated income verification; others require full docs. Some serve investment properties; others don't. Rate structures and origination fees vary widely. A broker compares multiple lenders and matches you with the best fit. Altgage's primary partner is Figure, but we also shop other lenders to ensure you get the best combination of rate, terms, and speed for your specific profile — whether that's maximum loan amount, fastest funding, lowest fees, or best rates.

What are Figure's key product features?

Figure is Altgage's primary HELOC partner. Key features include: loan amounts from $25K–$750K, competitive fixed rates locked at each draw, fully amortized terms (10, 15, 20, 30 years), no appraisal required for loans under $400K, no title insurance, no prepayment penalties, 5-day average funding, blockchain-powered automated underwriting, and availability in most states (not New York). Figure uses FICO 9 credit scoring, which is more favorable to borrowers with paid collections or rental history. All origination fees (0%–2.99%) are rolled into the loan — no cash due at closing.

The Bottom Line

A HELOC is one of the most versatile financial tools available to homeowners. It lets you access equity without selling your home, without refinancing your existing low-rate mortgage, and without the slow timelines of traditional home equity products.

Whether you're renovating, consolidating debt, bridging between homes, or building an investment portfolio, a HELOC gives you flexible, affordable access to capital. The key is understanding the terms — draw requirements, rate structures, CLTV limits, and lender-specific eligibility — and choosing the right product for your situation.

Altgage's primary HELOC partner is Figure, offering competitive fixed rates, fast funding, high CLTV limits, and seamless automated underwriting. But no single HELOC lender is best for every borrower. As a mortgage broker licensed in California, Massachusetts, Texas, Florida, Colorado, and Georgia, Altgage shops multiple HELOC and home equity lenders to find the best combination of rate, terms, and speed for your profile.

Related Reading on Altgage