A home equity line of credit (HELOC) and a home equity loan both let you borrow against the equity you've built in your home. But they work differently, cost differently, and fit different situations. The distinction, however, has gotten blurrier — modern HELOCs can now function much like traditional home equity loans, while offering unique structural advantages. For a full primer on how HELOCs work, see our complete HELOC guide.

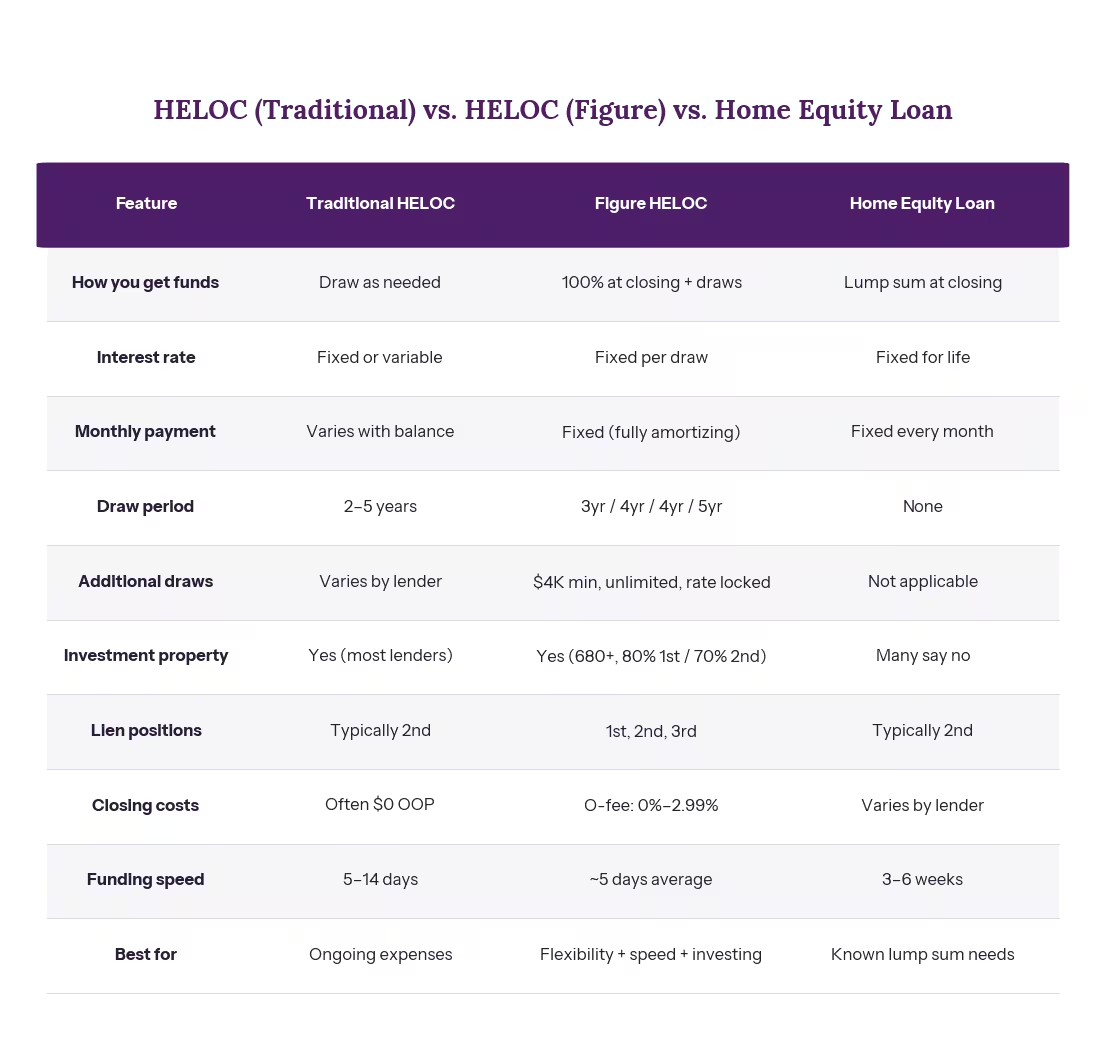

Here's the simplest framing: a home equity loan is like a personal loan secured by your house — a single lump sum at a fixed rate. A traditional HELOC is like a credit card secured by your house — a revolving credit line you draw from over time. But modern products (including Figure's HELOC, Altgage's primary HELOC partner) disburse 100% of funds at closing with a fixed rate per draw, making them structurally closer to home equity loans while preserving the draw period flexibility and investment property eligibility that traditional HELOCs offer. What matters isn't the product label but the specific terms.

The Core Differences at a Glance

How This Distinction Blurs: Figure's HELOC Model

Figure's HELOC operates differently from a traditional bank HELOC, and understanding this difference is key. Here's what sets it apart:

100% Initial Disbursement at Closing. Unlike a traditional HELOC that lets you draw $500 today and $5,000 next month, Figure disburses the full credit line amount upfront. This makes the initial funding behave like a home equity loan — you receive everything at once. However, you also get a draw period that extends 3–5 years depending on your term choice, during which you can request additional draws (minimum $4,000 each) at locked rates.

Fixed Rate Per Draw. Each time you draw (whether at closing or during the draw period), that portion locks in at a fixed rate. This eliminates the variable-rate risk that historically made HELOCs unpredictable.

Fully Amortizing from Day One. You're paying principal and interest immediately — no interest-only period that creates payment shock later.

Auto-Recast at 9.999% (No Fee). When your draw period ends, Figure automatically recalculates your payment based on the outstanding balance, so you don't have to requalify or refinance. If prime rate ever hits 9.999%, the recast is triggered automatically to prevent payment spike.

The bottom line: Figure's HELOC combines the initial funding certainty of a home equity loan with the flexibility, investment property eligibility, and faster closing of a modern HELOC.

How a Traditional HELOC Works

A traditional HELOC (with the flexibility to draw over time) has two phases:

Draw period (typically 2–5 years): You can borrow up to your credit limit, repay it, and borrow again — often requesting funds in increments. During this phase, most modern products are fully amortizing — you're paying both principal and interest from day one.

Repayment period (typically 12–27 years after the draw period): The draw period ends, you can no longer borrow, and you continue repaying the outstanding balance.

How a Home Equity Loan Works

A home equity loan is straightforward: you borrow a set amount, receive it all at closing, and repay it in fixed monthly installments over a fixed term — typically 10, 15, 20, or 30 years. There's no draw period, no revolving credit, and no payment variability.

This simplicity is its main advantage. You know exactly what you owe, what you'll pay each month, and when it will be paid off.

A few things to know about home equity loans:

- They are manually underwritten by some lenders, which means a human reviews your file. This can take longer but may allow for more flexibility on edge cases.

- Some lenders require a full appraisal rather than automated valuations (AVMs). This adds time and cost.

- Home equity loans are typically second-lien only — meaning you must have an existing first mortgage. If you own your home free and clear, a HELOC (which can sit in first lien position) may be your only option.

- Some lenders restrict home equity loans to primary residences and second homes. If you need to tap equity on an investment property, a HELOC is likely your only second-lien option.

Both HELOCs and home equity loans sit behind your first mortgage. In both cases, your first mortgage remains untouched — unlike a cash-out refinance, which replaces it entirely. Read our guide on HELOC vs. cash-out refinance for that comparison.

When to Choose a HELOC (Especially Figure)

You're funding a project with uncertain costs. Phased renovations rarely come in on budget. A HELOC draw period lets you access additional funds as needed. With Figure, you get 100% at closing for immediate access, plus the ability to draw additional funds (minimum $4,000 each) during the draw period at locked rates.

You need equity access on an investment property. This is critical. Many home equity loan lenders serve only primary residences. Figure explicitly supports investment properties with clear terms (680+ FICO, up to 80% LTV on a 1st lien, 70% on a 2nd or 3rd). If you're a real estate investor, this is a game-changer compared to traditional home equity loans.

You own your home free and clear or want a 1st/3rd lien position. Figure can sit in 1st, 2nd, or 3rd lien positions (3rd position limited to owner-occupied properties, 680+ FICO, 70% CLTV). Home equity loans are almost always 2nd lien. If you have no existing mortgage or want a superior lien position, Figure gives you options.

You want lower upfront costs and faster closing. Figure uses blockchain-enabled underwriting with automated valuations (no appraisal under $400K), no manual 1003 or document review, and 5-day average funding. You also get origination fee options ($0, 0.99%, 1.99%, 2.99%), so you can choose your cost structure. Traditional home equity loans often require full appraisals and take 3–6 weeks.

You may want to pay it down and redraw. Within the draw period, you can draw additional funds at the rate locked at the time of draw. This is perfect for phased projects or investors managing multiple property improvements.

You want transparency and fixed rates. Figure uses FICO 9 credit scoring, publicly underwritable parameters, and fixed rates per draw — no rate shopping black boxes or variable-rate surprises.

When to Choose a Home Equity Loan

You know exactly how much you need and want absolute payment certainty. If you're consolidating $45,000 in credit card debt with a single fixed monthly payment for a known term, a traditional home equity loan delivers that structure clearly.

You're disciplined about not re-borrowing. The revolving nature of a HELOC can tempt some borrowers to redraw after paying down. A home equity loan has no draw mechanism — it's a one-time funding event.

Your situation benefits from manual underwriting. Some home equity loan lenders will evaluate compensating factors (strong reserves, long employment, low overall debt) that automated systems might not weight favorably.

You need to refinance an existing HELOC. If your HELOC's draw period is ending and you want to lock in predictable payments without the draw period mechanics, refinancing into a fixed home equity loan is a common move.

The Rate Question

For current rates on Figure HELOCs and alternative home equity loan products, visit rates.altgage.com. Rates vary based on credit score, CLTV, property type, lien position, and loan amount. As a mortgage broker, Altgage shops multiple lenders to show you exact apples-to-apples comparisons.

Credit score matters significantly. Moving from a 660 to a 740 FICO can save you a full percentage point or more on either product. If you're in that range, consider a rapid rescore strategy before applying.

Altgage Perspective

Figure is Altgage's primary HELOC partner, offering speed, investment property eligibility, and multiple lien positions that traditional home equity loans don't provide. However, no single lender is best for every borrower. Figure has its own eligibility criteria (FICO 9 scoring, blockchain underwriting, up to $750K loan amount), while home equity loan lenders have different CLTV limits, credit score minimums, and property type restrictions. Altgage shops both Figure HELOCs and multiple home equity loan lenders to show you the best rate, payment, and total cost comparison for your specific situation. See your options at rates.altgage.com.

What About Closing Costs?

Home equity loans may have traditional closing costs including appraisal, title search, origination, and recording fees.

Figure's approach is more flexible. There's no appraisal under $400K (AVM-based), no title insurance, and no manual document review (blockchain underwriting). You choose your origination fee structure: 0%, 0.99%, 1.99%, or 2.99%. This transparency lets you compare total cost upfront rather than navigating variable lender fee structures.

For smaller loan amounts ($25,000–$50,000), the closing cost difference can tip the scale toward Figure even if another product has a slightly lower rate. For larger amounts, the rate differential matters more.

Figure-Specific Details

Loan Amounts. $25,000–$750,000.

Credit & FICO. Figure uses FICO 9 scoring and requires 680+ for standard products; lower minimums available. Investment properties require 680+ FICO with specific CLTV restrictions.

Underwriting. Blockchain-based underwriting, no 1003, no manual document requirements, no appraisal under $400K.

Draw Period by Term. Choose a term and get a corresponding draw period:

- 10-year term → 3-year draw period

- 15-year term → 4-year draw period

- 20-year term → 4-year draw period

- 30-year term → 5-year draw period

After the draw period closes, you enter the repayment period.

Additional Draws. Minimum $4,000 per draw; unlimited draws within the draw period. Each draw locks in at the rate offered at the time of draw.

Lien Positions. Figure can sit in 1st, 2nd, or 3rd lien positions. 3rd lien is owner-occupied only (680+ FICO, 70% CLTV max).

Investment Properties. Eligible at 680+ FICO, up to 80% LTV on a 1st lien, 70% on a 2nd or 3rd lien. LLC borrowers eligible for non-owner-occupied properties.

Funding. ~5 days average to closing.

No Co-Borrowers. Individual borrowers only.

Not Recommended For. Self-employed borrowers without standard income documentation.

Tax Deductibility

The tax treatment is identical for both HELOCs and home equity loans. Interest is deductible if the funds are used to buy, build, or substantially improve the home securing the loan, up to $750,000 in combined mortgage debt. If you use the funds for other purposes — debt consolidation, education, business — the interest is not deductible. Consult a tax professional for your specific situation.

Frequently Asked Questions

Is a HELOC the same as a home equity loan?

Not in the traditional sense. But modern HELOCs like Figure's now blur the line. A traditional HELOC provides a revolving credit line with a draw period. A home equity loan is a one-time lump sum. Figure's HELOC disburses 100% upfront (like a home equity loan) but offers a draw period for additional borrowing (like a traditional HELOC), combining the advantages of both structures.

Which has a lower interest rate: HELOC or home equity loan?

It depends on the specific lender, your credit profile, and current market conditions. See rates.altgage.com for side-by-side rate quotes.

Can I convert a HELOC to a home equity loan?

You would need to close the existing HELOC and open a new home equity loan. Some lenders offer streamlined refinancing for this transition. If your HELOC's draw period is ending and you want locked payments without draw mechanics, a home equity loan refinance is a common move.

Which is better for debt consolidation?

Both work. A home equity loan is better if you know the exact amount and want a single fixed payment. A HELOC is better if you're paying off multiple debts over time or want flexibility.

Can I have both a HELOC and a home equity loan?

It depends on lender requirements. Some home equity loan lenders require that all existing liens (except your first mortgage) be paid off at closing. Others allow stacking. With Figure, you can have multiple draws within the draw period on the same HELOC, effectively acting as multiple advances. Altgage can help you figure out which combinations work for your situation.

Which is faster to get?

Figure HELOCs fund in ~5 days average using automated underwriting. Traditional home equity loans often take 3–6 weeks, especially with manual underwriting and in-person appraisals.

Can I use either product on an investment property?

Figure HELOCs explicitly support investment properties with clear underwriting parameters. Many home equity loan lenders restrict to primary residences and second homes only. If you need a second-lien product on a rental property, Figure is a stronger option than traditional home equity loans.

The Bottom Line

The choice between a HELOC and a home equity loan isn't just about the product label anymore. Figure's HELOC offers 100% upfront funding like a home equity loan, but with fixed rates, a draw period for flexibility, investment property eligibility, multiple lien positions, and faster closing — advantages that traditional home equity loans often don't provide.

If you need flexible, ongoing access to equity — especially on an investment property, a home you own free and clear, or a project with uncertain scope — a HELOC (and specifically Figure's model) is the better tool. If you need a specific amount with locked-in payments and no temptation to reborrow, a home equity loan gives you that structure.

Both products protect your existing first mortgage rate — neither requires you to refinance. Both offer rates dramatically lower than credit cards or personal loans. The right choice depends on how you plan to use the funds, your property type, and how much flexibility you need.

Altgage sources Figure HELOCs and home equity loans from multiple lenders, each with different eligibility criteria and pricing. See your options at rates.altgage.com.

Related Reading on Altgage