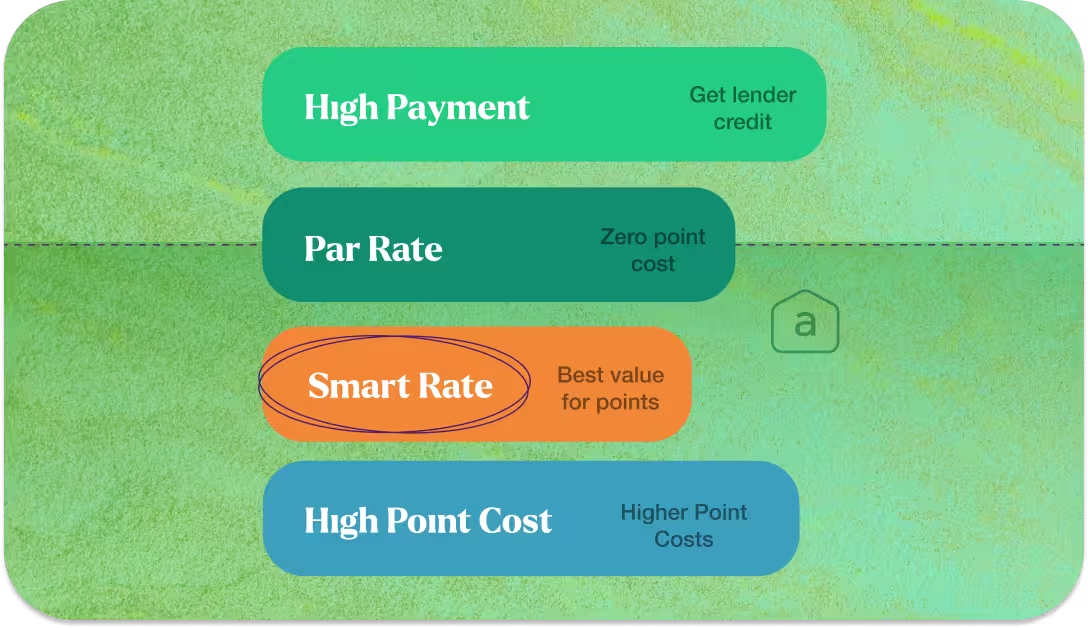

Your lender offers you a choice: take a 6.75% rate, or pay some money upfront to get 6.50%. Or 6.25%. Maybe even 6.00%. Each step down costs you—and each step saves you money every month for the life of the loan.

These upfront payments are called mortgage points (or discount points), and they're one of the most misunderstood tools in the mortgage process. Paying points is essentially prepaying interest—and whether it's worth it depends entirely on your math, not your lender's sales pitch.

What Are Mortgage Points?

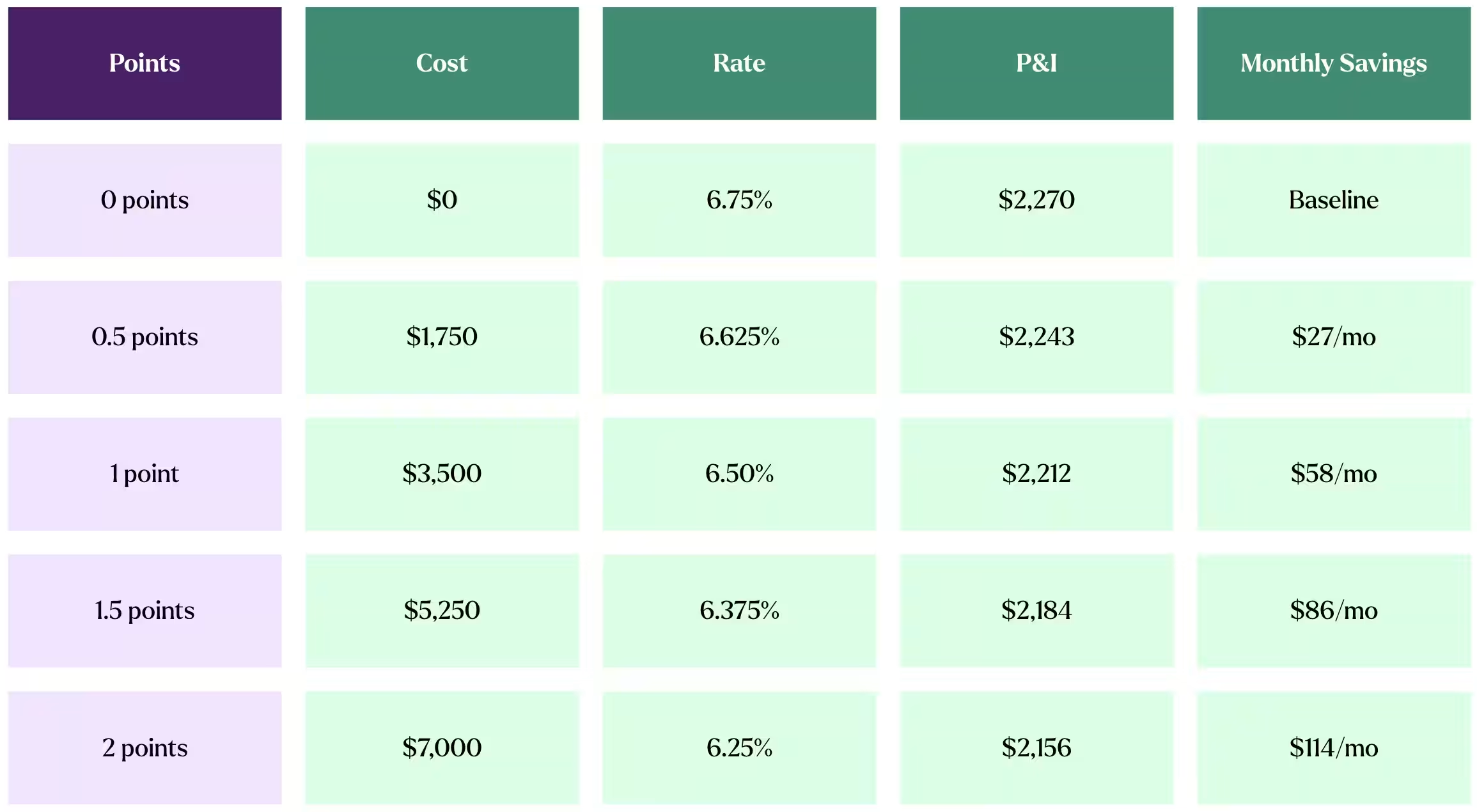

A mortgage point equals 1% of your loan amount. On a $350,000 loan, one point costs $3,500. Each point you buy typically reduces your interest rate by approximately 0.25%, though the exact reduction varies by lender and market conditions.

There are two types of points:

Discount Points (What Most People Mean)

Discount points are optional fees you pay at closing to reduce your interest rate. This is "buying down" your rate. The more points you buy, the lower your rate goes. Here's our calculator to see your breakeven and how much you'll save over tiime

Origination Points (Lender Fees)

Origination points are fees the lender charges for processing your loan. These are a cost of getting the loan and do not reduce your rate. When people talk about "paying points," they almost always mean discount points.

Don't confuse the two. When comparing loan estimates from different lenders, look specifically at discount points (rate buydown) versus origination fees (lender charges). A lender advertising a lower rate may be charging more in origination points, making the total cost comparable.

How Discount Points Reduce Your Rate

The Breakeven Calculation: The Only Math That Matters

The breakeven formula is straightforward, a.

Breakeven (months) = Upfront point cost ÷ Monthly payment savings

Using our example of 1 point ($3,500) saving $58/month:

$3,500 ÷ $58 = 60 months = 5 years

If you keep the loan for more than 5 years, buying the point saves you money. If you sell or refinance before 5 years, you've lost money on the deal.

Notice that the breakeven is roughly 5 years regardless of how many points you buy. The decision isn't about how many points to buy—it's about whether you'll keep the loan past the breakeven point.

When Buying Points Makes Sense

- You're staying in the home for 7+ years: You'll be well past breakeven, and the cumulative savings grow every year.

- You won't refinance unless rates drop significantly: Refinancing resets the clock.

- You have excess cash beyond down payment and reserves: Points should come from surplus funds.

- You want to maximize tax deductions in the purchase year: Discount points are generally tax deductible in the year they're paid on a purchase.

- You're prioritizing lowest possible monthly payment: Points reduce your ongoing obligation.

When Buying Points Doesn't Make Sense

- You might move in 3–5 years: You won't reach breakeven.

- You're likely to refinance soon: If rates are historically high and you expect to refinance when they drop, paying points on a temporary rate is wasteful.

- It would deplete your cash reserves: Never sacrifice your emergency fund for points.

- The invested alternative earns more: If you could invest that $3,500 and earn more than the equivalent of 0.25% rate savings, the math favors investing.

- You're buying a starter home: First homes are often held 3–7 years. The probability of not reaching breakeven is higher.

Points vs. Lender Credits: Opposite Strategies

Buy points — Upfront Cost: Higher (you pay points) | Monthly Payment: Lower | Best For: Long-term holds (7+ years)

No points — Upfront Cost: Baseline | Monthly Payment: Baseline | Best For: Medium holds (5–7 years)

Lender credit — Upfront Cost: Lower (lender pays your costs) | Monthly Payment: Higher | Best For: Short holds (1–5 years)

Are Mortgage Points Tax Deductible?

Generally, yes—with some important caveats:

- Purchase vs Refi loans: Points paid on a purchase mortgage are typically fully deductible in the year paid but points on a refinance must be amortized over the life of the loan, not in a single year.

- Standard deduction consideration: Points are only useful as a deduction if you itemize your tax deductions. With increased standard deductions after the Tax Cuts and Jobs Act, most couples filing jointly may not be able to item

- Seller Paid points: are tax deductible but must be subtracted from the home's cost basis

Points are reported on Schedule A (Form 1040) and found on Form 1098. Always consult a tax professional for your specific situation.

Frequently Asked Questions

How many points can I buy?

Most lenders allow you to buy up to 3–4 points, though the rate reduction per point typically diminishes after the first 1–2 points. The practical sweet spot is usually 0.5 to 1.5 points.

Can the seller pay for my points?

Yes, as part of seller concessions. This is subject to the same concession limits by loan type (3–9% for conventional, 6% for FHA, 4% for VA).

Do points make sense in a high-rate environment?

Be cautious. If rates are historically high and you expect them to decline, you're likely to refinance—which resets the breakeven clock. Taking the higher rate now and refinancing later often makes more sense.

Is buying points the same as making a bigger down payment?

No. A bigger down payment reduces your loan amount. Points reduce your rate but keep the same loan amount. Both reduce your monthly payment, but through different mechanisms.

The Bottom Line

Mortgage points are a straightforward financial tool: pay cash upfront, get a lower rate for the life of the loan. The math is simple—breakeven is typically 5–6 years. If you're staying longer, points save you money. If you're not, they don't. The key is running your specific numbers, not guessing. At Altgage, we show you the math for your specific scenario so you can decide with clarity, not speculation. See your numbers at rates.altgage.com.