You spent 30 years paying off your mortgage. Now the house is yours—free and clear—and it’s probably worth more than you ever expected. But here’s the problem: that wealth is locked inside the walls. You can’t spend your roof.

A reverse mortgage changes that. It lets homeowners 62 and older convert a portion of their home equity into usable cash—without selling the house, without moving, and without making monthly mortgage payments. The most common type is a Home Equity Conversion Mortgage (HECM), which is insured by the Federal Housing Administration (FHA) and regulated by HUD.

If that sounds too good to be true, you’re not alone. Reverse mortgages carry decades of stigma from the pre-2008 era, when consumer protections were weaker and the products were often misunderstood. Modern reverse mortgages are fundamentally different—they’re regulated, non-recourse, and increasingly used as legitimate retirement planning tools by financial advisors nationwide.

This guide explains how reverse mortgages work, what they cost, who qualifies, and how to decide if one makes sense for your retirement.

How a Reverse Mortgage Works

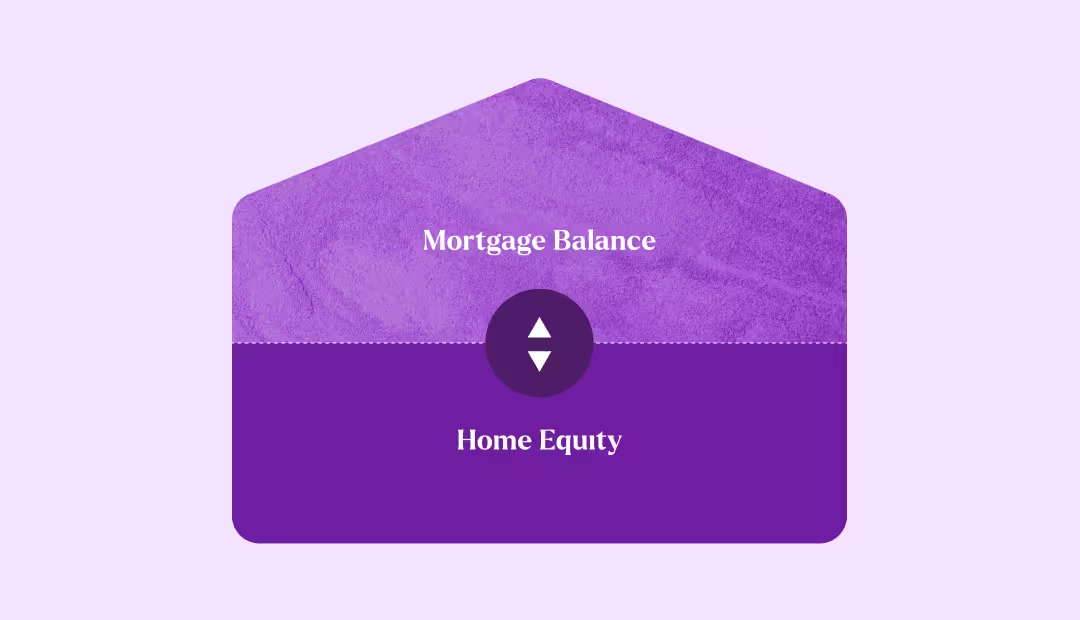

A reverse mortgage is the mirror image of a traditional (or “forward”) mortgage. With a forward mortgage, you start with a large loan balance and make monthly payments to reduce it over time, building equity as you go. With a reverse mortgage, you start with equity and convert it into loan proceeds—and the loan balance grows over time instead of shrinking.

Here’s the key: you don’t make monthly mortgage payments on a reverse mortgage. Interest and fees accrue on the loan balance, and the full amount becomes due only when the last borrower leaves the home—whether by selling, moving to assisted living, or passing away.

The borrower retains full ownership of the home throughout the life of the loan. You stay on the title, you make decisions about the property, and you can sell at any time. The reverse mortgage is simply a lien against the property—just like any other mortgage.

Forward Mortgage vs. Reverse Mortgage

Understanding the core differences:

Monthly payments: A forward mortgage requires monthly principal and interest payments. A reverse mortgage requires none

Loan balance over time: Forward mortgages decrease. Reverse mortgages increase as interest accrues

Home equity over time: Forward mortgages build equity through payments. Reverse mortgages draw down equity (though home appreciation can offset this)

Who receives payments: With a forward mortgage, you pay the lender. With a reverse mortgage, the lender pays you

When the loan is repaid: Forward mortgages are repaid over 15–30 years via monthly payments. Reverse mortgages are repaid when the borrower leaves the home

Age requirement: Forward mortgages have no age requirement (18+ to sign). HECMs require the primary borrower to be 62+

Non-recourse protection: HECMs are non-recourse—you and your heirs can never owe more than the home’s fair market value

Types of Reverse Mortgages

HECM (Home Equity Conversion Mortgage)

The HECM is the most common reverse mortgage in the United States, accounting for roughly 90% of all reverse mortgage originations. It’s insured by the FHA and available through FHA-approved lenders, including mortgage brokers like Altgage.

HECMs have a lending limit of $1,249,125 in 2026 (set annually by HUD). The actual amount you can borrow depends on your age, home value, and current interest rates—calculated using a formula called the principal limit factor (PLF). Generally, older borrowers with more valuable homes and lower rates can access more equity.

HECMs offer multiple disbursement options: a lump sum, a line of credit, monthly payments (tenure or term), or a combination. The line of credit option is increasingly popular because the unused portion grows over time at the same rate charged on the loan balance—effectively giving you access to more equity the longer you wait to use it.

Proprietary (Jumbo) Reverse Mortgages

For homeowners with properties valued above the HECM limit, proprietary reverse mortgages offer loan amounts up to $4 million. These are private products—not FHA-insured—offered by specific lenders like Finance of America (their HomeSafe product line). Proprietary products often have a lower minimum age (55+ in most states vs. 62 for HECM) and don’t charge FHA mortgage insurance premiums.

The trade-off: proprietary products don’t include the HECM’s unique line-of-credit growth feature, and they may have different rate structures. As a mortgage broker, Altgage can help you compare HECM and proprietary options side by side to determine which fits your situation.

HECM for Purchase

A lesser-known option, the HECM for Purchase lets you buy a new primary residence using reverse mortgage proceeds combined with a down payment. This is particularly useful for retirees who want to downsize, relocate, or move closer to family without taking on monthly mortgage payments in the new home.

Who Qualifies for a Reverse Mortgage?

To be eligible for an FHA-insured HECM, you must:

- Be 62 years of age or older (the primary borrower; a younger non-borrowing spouse has certain protections).

- Own your home outright or have a low remaining mortgage balance that can be paid off with the reverse mortgage proceeds.

- Live in the home as your primary residence.

- Not be delinquent on any federal debt (such as federal student loans or tax liens).

- Complete a HUD-approved reverse mortgage counseling session before applying. This is mandatory and costs approximately $125.

- Demonstrate the financial ability to maintain the home, pay property taxes, and keep homeowners insurance current. Lenders verify this through a financial assessment.

Eligible property types include single-family homes, 2–4 unit properties (if you live in one unit), FHA-approved condominiums, and some manufactured homes. Co-ops and most vacation homes are not eligible.

Altgage Perspective: Many homeowners assume they won’t qualify because they still have a mortgage balance. In most cases, the reverse mortgage pays off the existing forward mortgage first—the remaining proceeds go to you. If you owe $80,000 on a home worth $400,000, you may still access a significant portion of your equity. Talk to an Altgage reverse mortgage specialist to see your specific numbers.

How You Receive the Money

One of the most misunderstood aspects of reverse mortgages is how borrowers actually receive funds. You have several options, and choosing the right one matters:

Lump Sum

A one-time payment at closing. Only available on fixed-rate HECMs, and limited to 60% of the principal limit in the first year. Best for paying off an existing mortgage or covering a large one-time expense.

Line of Credit

Draw funds as needed over time. The unused portion grows at the same rate as the loan’s interest plus the annual MIP—so your available credit increases even if you don’t touch it. This is the most flexible option and the one most commonly recommended by financial planners. Best for supplementing retirement income, building emergency reserves, or implementing a coordinated withdrawal strategy.

Tenure Payments

Equal monthly payments for as long as you live in the home. These payments continue even if you outlive the loan balance—the FHA insurance guarantees them. Best for replacing a pension-like income stream.

Term Payments

Equal monthly payments for a fixed number of months that you choose. Best for bridging a specific income gap, such as funding expenses from age 62 until Social Security kicks in at 70.

Combination

A mix of line of credit with tenure or term payments. Best for maximum flexibility with some guaranteed monthly income.

The line of credit deserves special attention. Unlike a traditional home equity line of credit (HELOC), a reverse mortgage LOC cannot be frozen or reduced by the lender—even if your home value drops. And the unused portion grows at the same rate as the loan’s interest charge plus the annual mortgage insurance premium. This growth feature is unique to the HECM program and is one of the reasons financial planners increasingly view it as a strategic retirement tool.

What Does a Reverse Mortgage Cost?

Reverse mortgages aren’t free. Understanding the costs is essential to determining whether one makes financial sense for you.

Upfront Costs

Mortgage Insurance Premium (MIP): 2% of your home’s appraised value (or the HECM limit, whichever is lower), paid at closing. On a $400,000 home, that’s $8,000. This premium funds the FHA insurance that protects you and your heirs with non-recourse protection.

Origination Fee: Lenders can charge up to $6,000, calculated as the greater of $2,500 or 2% of the first $200,000 of home value plus 1% of the value above $200,000. Some brokers offer reduced origination fees—it’s worth comparing.

Closing Costs: Standard third-party costs including appraisal ($400–$600), title insurance, recording fees, and other settlement charges. These are similar to any mortgage closing.

Counseling Fee: Approximately $125 for the mandatory HUD-approved counseling session. This is often the only out-of-pocket cost before closing, as most other fees can be financed into the loan.

Ongoing Costs

Annual MIP: 0.5% of the outstanding loan balance per year, charged monthly. This accrues onto the loan balance.

Interest: Accrues on the outstanding balance. HECM rates are typically based on a margin plus an index (such as the 1-year CMT). As of early 2026, expected rates on adjustable-rate HECMs generally range from the mid-5% to mid-7% range depending on the margin and index—but rates change frequently, so check current pricing.

Servicing Fee: Some lenders charge a monthly servicing fee (up to $35), though many have eliminated this or rolled it into the margin.

Important: You don’t have to pay most of these fees out of pocket. The MIP, origination fee, and closing costs can be financed into the loan proceeds. This reduces your available equity but eliminates the need for cash at closing. The trade-off is that financed costs accrue interest over the life of the loan.

Common Myths About Reverse Mortgages

The biggest obstacle to reverse mortgage adoption isn’t cost or eligibility—it’s stigma. Much of what people “know” about reverse mortgages comes from the pre-2008 era. Here’s the reality in 2026:

The Bank Takes Your Home

Reality: You remain on the title for the entire life of the loan. The lender has a lien on the property (just like any mortgage), but you own the home. You can sell at any time, and your heirs inherit the home subject to the loan balance.

You Can End Up Owing More Than Your Home Is Worth

Reality: HECMs are non-recourse loans. This means that neither you nor your heirs will ever owe more than the home’s fair market value at the time of repayment. If the loan balance exceeds the home value, FHA insurance covers the difference. This is one of the most important consumer protections in the program.

Reverse Mortgages Are a Last Resort

Reality: This perception is outdated. A growing body of peer-reviewed research—including studies published in the Journal of Financial Planning—shows that strategically using a reverse mortgage line of credit can extend retirement portfolio longevity and increase legacy wealth. Financial advisors increasingly recommend them as part of a coordinated retirement income strategy, not as a desperation measure.

Reverse Mortgages Are Like Subprime Loans From 2008

Reality: Modern HECMs require mandatory counseling, financial assessments, and are insured by the FHA. Borrowers must demonstrate the ability to maintain property taxes and insurance. These protections didn’t exist (or were weaker) before 2015. The product has been substantially reformed.

Your Heirs Will Be Stuck With the Debt

Reality: When the loan becomes due, heirs have options: sell the home and keep any equity above the loan balance, refinance the reverse mortgage into a forward mortgage to keep the home, or simply walk away with no personal liability (non-recourse protection). Heirs are never personally responsible for the debt.

Reverse Mortgages as a Retirement Planning Tool

This is where the conversation shifts from “what is it” to “why it matters.” For homeowners with significant equity and a retirement portfolio, a reverse mortgage—particularly the line of credit option—can serve as a powerful complement to traditional retirement income strategies.

Eliminating Monthly Mortgage Payments

If you still carry a forward mortgage in retirement, a reverse mortgage can pay it off and eliminate the monthly payment. For a household paying $1,800/month on a remaining mortgage balance, that’s $21,600 per year returned to cash flow—without selling the home.

Supplementing Income Without Selling Investments

When the stock market drops, selling investments to fund living expenses locks in losses and accelerates portfolio depletion. This is known as sequence of returns risk—the biggest threat to retirement portfolios. Drawing from a reverse mortgage line of credit during down markets instead of your 401(k) or IRA gives your investments time to recover.

Delaying Social Security

Every year you delay Social Security past age 62, your benefit increases by approximately 6–8% per year, up to age 70. Reverse mortgage proceeds can bridge the income gap, funding living expenses from age 62 to 70 while your Social Security benefit compounds. The math on this strategy can be compelling.

The Coordinated Withdrawal Strategy

A growing body of academic research supports what’s called the “coordinated withdrawal strategy”: opening a HECM line of credit at the start of retirement and drawing from it during years when your investment portfolio declines. When the portfolio recovers, you repay the LOC (or leave it outstanding). Multiple studies show this approach can extend portfolio life by 5+ years and increase net legacy wealth compared to the conventional approach of saving home equity as a last resort.

We explore this strategy in depth in our guide: The Coordinated Withdrawal Strategy: Using a Reverse Mortgage to Extend Your Retirement Portfolio.

How to Get a Reverse Mortgage

The process typically takes 30–45 days from application to closing:

Step 1: HUD-Approved Counseling

Before you can apply, you must complete a counseling session with a HUD-approved reverse mortgage counselor. This is mandatory and takes about an hour. The counselor will explain how the product works, review your financial situation, and ensure you understand the obligations. Cost is approximately $125 and can be done by phone.

Step 2: Application and Financial Assessment

Your lender will review your financial profile: credit history, income, property tax payment history, and insurance. This isn’t about qualifying based on income (like a forward mortgage)—it’s about confirming you can maintain the home and pay property charges going forward.

Step 3: Home Appraisal

An FHA-approved appraiser determines your home’s current market value. This establishes the maximum claim amount and, combined with your age and current interest rates, determines how much you can borrow.

Step 4: Underwriting and Approval

The lender underwrites the loan, verifies all documentation, and issues a commitment. This typically takes 2–3 weeks.

Step 5: Closing

You sign closing documents (similar to any mortgage closing). There’s a 3-business-day right of rescission after closing, during which you can cancel without penalty.

Step 6: Disbursement

After the rescission period, funds are disbursed according to your chosen option. If you have an existing mortgage, it’s paid off first from the proceeds.

Your Obligations as a Borrower

A reverse mortgage doesn’t mean “free money.” You have ongoing responsibilities:

Property taxes must be paid on time. Delinquent property taxes can trigger a loan default.

Homeowners insurance must be maintained continuously.

Home maintenance: The property must be kept in reasonable condition.

Primary residence: You must live in the home as your primary residence. Leaving for more than 12 consecutive months (e.g., moving to assisted living) can trigger repayment.

HOA fees, if applicable, must be kept current.

If you fail to meet these obligations, the lender can call the loan due. In some cases, lenders will set aside a portion of proceeds in a Life Expectancy Set-Aside (LESA) to cover property taxes and insurance if the financial assessment identifies risk.

Frequently Asked Questions

Is a reverse mortgage the same as a HECM?

Not exactly. A HECM is a specific type of reverse mortgage insured by the FHA and regulated by HUD. It’s the most common type, but proprietary (jumbo) reverse mortgages also exist for homes above the FHA lending limit. When most people say “reverse mortgage,” they mean a HECM.

Can I get a reverse mortgage if I still have a mortgage?

Yes. The reverse mortgage pays off your existing mortgage first, and you receive the remaining proceeds. You need enough equity for the reverse mortgage to cover the existing balance and still leave you with meaningful funds.

How much money can I get from a reverse mortgage?

It depends on three factors: your age (older = more), your home’s appraised value (up to the 2026 HECM limit of $1,249,125), and current interest rates (lower = more). A 72-year-old with a $500,000 home might qualify for roughly $250,000–$300,000 in proceeds, but this varies significantly. Get a personalized estimate from an Altgage specialist.

Do I pay taxes on reverse mortgage proceeds?

Generally, no. Reverse mortgage proceeds are considered loan advances, not income, so they are typically not subject to federal income tax. This makes them tax-efficient compared to withdrawals from pre-tax retirement accounts. However, consult a tax professional for your specific situation.

What happens to my reverse mortgage when I die?

The loan becomes due. Your heirs have several options: sell the home and keep any equity above the loan balance, refinance into a forward mortgage to keep the home, or walk away with no personal liability. The loan is non-recourse—heirs never owe more than the home’s fair market value.

Can a reverse mortgage affect my Social Security or Medicare?

Reverse mortgage proceeds generally do not affect Social Security retirement benefits or Medicare. However, if you receive Medicaid or Supplemental Security Income (SSI), unspent reverse mortgage proceeds held in your bank account could count as an asset and potentially affect eligibility. Spend or allocate the funds within the same calendar month to avoid this issue.

How does a reverse mortgage compare to a HELOC?

Key differences: HELOCs require monthly payments and can be frozen by the lender. Reverse mortgages require no monthly payments and the line of credit cannot be frozen or reduced. However, reverse mortgages have higher upfront costs, are only available to homeowners 62+, and the loan balance grows over time. We compare them in detail in our Reverse Mortgage vs HELOC guide.

What is the 2026 HECM lending limit?

The 2026 national HECM lending limit is $1,249,125, up from $1,209,750 in 2025. This means your home value up to this amount is used to calculate your available proceeds. If your home is worth more, consider a proprietary reverse mortgage for access to higher amounts.

The Bottom Line

A reverse mortgage is a tool—not a lifeline and not a scam. For the right homeowner, it unlocks wealth that’s otherwise inaccessible, eliminates monthly mortgage payments, and provides flexibility that no other financial product offers to retirees. For the wrong homeowner, the costs outweigh the benefits.

The key questions to ask yourself: Do I plan to stay in my home for the foreseeable future? Do I have significant equity? Could I benefit from additional cash flow or a financial safety net in retirement? If the answer to all three is yes, a reverse mortgage is worth exploring.

At Altgage, we believe in transparent comparison. We’ll show you the numbers on a HECM, compare it against proprietary products like HomeSafe, and help you understand exactly what you’d receive and what it would cost—before you commit to anything. Start with a no-obligation conversation at https://calendly.com/sukesh-altgage/1-on-1